Is this the new era? Funding for sexual & reproductive health R&D 2018-2023

By Impact Global Health 30 April 2025

What this report tells us

- Funding for sexual & reproductive health R&D has grown rapidly since we began tracking it in 2018, nearly doubling from $451m to $889m, though this is partly due to an increase in the conditions we include

- Increased funding has focused on STIs, while contraceptive R&D has tumbled, as shifting private sector priorities have left a big gap in contraceptive product development

- Overall growth in SRH R&D has been driven by funding for platform technologies, which will need to be adapted to specific pathogens before they can make an impact

- Female-only conditions remain the most significant area of neglect, receiving only a small share of SRH funding

- The high proportion of basic research funding and small shares for clinical development in women’s health show how far we have left to go to develop new products

- The US NIH, the Gates Foundation, and the pharmaceutical industry accounted for 82% of global SRH funding in 2023, and an even larger share of SRH-specific R&D

- The US government plays – or played – a critical role in funding SRH R&D: what happens next will have a big impact on the SRH R&D landscape going forward

US government-dominated funding, and a focus on basic research and platform technologies means there is a large and growing need for late-stage funding to turn discoveries, platforms and candidates into actual products

Number of major funders vs share of funding provided by the US NIH, 2023

Sexual & reproductive and women’s health: A new era?

Sexual and reproductive health spans a variety of needs and issues over a person’s lifetime. This starts in adolescence (including menarche), journeys through reproductive years (encompassing issues such as sexually transmitted infections, reproductive cancers, contraception, abortion, maternal health, as well as chronic gynaecological conditions like endometriosis, polycystic ovary syndrome and uterine fibroids), and into mature or post-reproductive life (such as menopause).

While the concept of sexual & reproductive health covers issues relevant to both sexes, it is also true that many SRH issues affect women and girls exclusively, or they affect them disproportionately or in a different way to men and boys. So, although ‘women’s health’ is a broad concept that includes a wide range of issues (from infectious diseases, non-communicable diseases, to chronic conditions and beyond), the intersection between SRH and women’s health is, undoubtedly, significant. It is within this broader framework of women’s health that this report now sits, recognising this critical gender dimension, and its implication on the development of biomedical products to meet their needs. Indeed, while commercial failures plague R&D for LMIC contexts, SRH and women’s health issues also bear the brunt of systemic gender-related biases in medical and biomedical research. This translates to critical market failures for SRH and women’s health products and technologies in general, which is compounded for those that are also appropriate for use in LMICs.

Promisingly, in the last few years a wave of momentum towards championing women’s health, and particularly questioning the historical neglect of women and girls in medical research altogether, has borne fruit. The FemTech industry is booming to an estimated worth upwards of $1 billion, women’s heath stakeholders globally have come together to lay out pathways for progress, and philanthropic organisations and governments had made commitments to turn the tide. Until very recently, this upward trend was the new era in women’s health. But, in the context of a new geopolitical direction less supportive of gender-responsive research, the last few months have left the future of women’s health R&D uncertain. And this, now, is the new era in women’s health.

At this critical time – when information is sorely needed to help shape the direction of women’s health R&D, especially within the global health context – this report offers key insights on trends in global investments in SRH and women’s health R&D.

What's in this report

This is the fourth in a series of reports from Impact Global Health summarising the state of global funding for LMIC-applicable biomedical research and development targeting a range of sexual & reproductive health and women’s health issues – which we collectively abbreviate as SRH – based on data gathered via the G-FINDER survey of R&D funding.

This report provides a summary of the investments made between 2018 and 2023, measured in 2023 US dollars (‘US$’), across each of the conditions included in our scope. Additional analyses are available in our accompanying report focused on gynaecological conditions, which also draws from our comprehensive pipeline data to contextualise the funding landscape within the broader R&D ecosystem for those issues. Brief insights are also available on the disease/condition pages on our website for the individual SRH issues covered in this report.

Graphs and tables based on the underlying investment data used in creating this report can be generated using our online data portal, while interactive pipeline and approved product data can be accessed in our R&D tracker.

While the conditions included in the report remained unchanged between 20181 and 2022 – providing five years of consecutive trend data – several new women’s health conditions were added to the scope in 2023 following an extensive consultation with our women’s health expert advisory group. These were identified based on a broad review of women’s health conditions filtered and prioritised using the following five criteria:

The additional conditions added were endometriosis, polycystic ovary syndrome, uterine fibroids, menopause, maternal iron deficiency anaemia, preterm labour and abortion. The 2023 increase in headline funding should be viewed in this context, and we explain how to interpret the headline totals in light of this change in the following section. For a detailed breakdown of all diseases, products and types of research activity included, please refer to our R&D scope document.

Year-to-year differences in survey participation can also lead to artefactual changes in reported funding. Participation has remained relatively consistent overall including 2023, with most of the changes affecting our aggregate (for confidentiality reasons) measure of industry funding. We will highlight places where participation changes significantly influence our results in the sections below.

Inflation adjustments and industry data

Funding data is adjusted for inflation and converted to US dollars to eliminate artefactual effects caused by inflation and exchange rate fluctuations.

All pharmaceutical industry funding data is aggregated and anonymised for confidentiality, with a distinction made between multinational pharmaceutical companies (‘MNCs’) and small pharmaceutical and biotechnology firms (‘SMEs’).

What’s not included

The purpose of G-FINDER is to track and analyse global investment in R&D of new health technologies for global health issues, including SRH; it is not intended to capture investment in the entire spectrum of global health or SRH research. Significant investments in health systems and operational/implementation research and sociological, behavioural and epidemiological research not related to the development of new health technologies are not included in our funding totals. Similarly, funding for health programme delivery, advocacy, and general capacity building to address global health falls outside the scope of G-FINDER.

In the following sections, we occasionally omit some qualifiers for the sake of readability: we might talk about ‘funding for STIs’, for example, but our funding totals only ever refer to R&D funding – not funding for STI prevention or treatment generally. Similarly, we might occasionally talk about ‘this year’s funding total’ in reference to funding for 2023 – the period covered by the latest G-FINDER survey – and ‘last year’ therefore refers to 2022.

Figure 1 – funding by disease and year, 2018-2023

1 The 2018 report included coverage of hepatitis B and HIV, both of which are now covered exclusively in our annual G-FINDER reports on neglected disease R&D.

Overview of the funding landscape

Growth in headline funding is mostly the result of scope expansion, and funding for STIs & platform technologies

Funding for SRH R&D reported through G-FINDER has grown rapidly since we began tracking it in 2018, nearly doubling from $451m in 2018 to $889m in 2023 – the most recent year for which we have data.

Prior to 2023, overall funding had trended upwards by nearly $50m a year, lifting overall funding by 45% between 2018 and 2022.

This long-term upwards trend, and especially the sharp increase in 2023 funding (a rise of $233m, or 36%) though, overstates the actual rate of growth for two reasons: first, we began including several new women’s health conditions2 in our survey in 2023. These conditions received a total of $117m in 2023, meaning that as much as 27% of our long-term funding growth may just be an artefact of this survey expansion.

Second, a little under half of the growth (another $205m of the long-term $438m increase) was in the form of increased non-issue-specific (or ‘NIS’) funding. This is mostly funding for areas applicable to multiple global health areas – neglected disease and emerging infectious disease alongside SRH – such as platform technologies (tools or methods which can be used to develop multiple different products efficiently and cost effectively) or core funding to organisations which support SRH alongside other kinds of R&D. Since these technologies are mostly backed by funders focusing on their application to emerging infectious diseases like COVID, they will require further development to adapt them to sexual and reproductive health.

Setting this aside, funding for the SRH conditions consistently included in our survey since 2018 has grown by a slightly less impressive $115m (26%), with a little over half that growth happening in 2023 alone. The largest areas of growth were sexually transmitted infections3 – up $122m, or 127% between 2018 and 2023 – and human papillomavirus (HPV) & HPV-related cervical cancer R&D, which grew by $25m (25%) between 2018 and 2023. These figures slightly exaggerate the share of the growth that happened in 2023 specifically, since over $20m is funding from entirely new survey participants whose research began after 2018 but for whom we have only 2023 data.

Funding for both contraception and multipurpose prevention technologies (MPTs) has fallen a lot since 2018, with contraceptive R&D down $18m (-15%) and MPTs by $35m (-55%). Meanwhile, funding for abortion, maternal health and gynaecological conditions remains dismally low, ranging from $35m for preterm labour, to just $2.8m for maternal iron deficiency anaemia, to a mere $1.1m for abortion R&D.

Figure 2 – funding by condition and year, 2018-2023

2 Endometriosis, polycystic ovary syndrome, uterine fibroids, menopause, maternal iron deficiency anaemia, preterm labour & abortion.

3 This includes herpes simplex virus 2, gonorrhoea, chlamydia, syphilis, HTLV-2 and catchall categories for multiple and other STIs.

Sexually transmitted infections

Funding for STIs has more than doubled since 2018, while HPV funding grew a little more slowly

This section covers funding for sexually transmitted infections included in our overarching ‘STIs’ category: herpes simplex virus 2 (HSV-2), gonorrhoea, chlamydia, syphilis, human T-lymphotropic virus 1 (HTLV) as well as categories for R&D to address multiple STIs concurrently, and a catchall category for other STIs. It also covers human papillomavirus & HPV-related cervical cancer R&D, although it is collected and treated as a distinct category due to the inclusion of cancer-related R&D. Some other STIs and diseases susceptible to sexual transmission – including HIV, hepatitis B & C, and Zika – are covered separately in our reports on neglected or emerging infectious disease R&D.

Globally, more than one million STIs are acquired daily among people aged 15-49. While most STIs are not life-threatening, timely diagnosis and treatment is crucial to avoiding further transmission and long-term complications like pelvic inflammatory disease, infertility and cancers, which affect women disproportionately. Affordable point-of-care testing is essential for early intervention and limiting transmission, especially in LMICs. Critically, some previously treatable STIs such as gonorrhoea are now showing widespread antibiotic resistance (‘antimicrobial resistance’ or AMR) and are posing serious public health challenges globally. New drug regimens and diagnostics capable of detecting resistant strains are needed to keep ahead of the curve. There are still no vaccines against chlamydia, HSV-2, HTLV-1, syphilis or gonorrhoea but their development could greatly improve prevention strategies. Therapeutic vaccines, especially for HSV-2 which has currently no cure, could significantly reduce STIs’ global burden. Microbicides could also improve prevention strategies, particularly for protection against multiple pathogens and/or pregnancy, with products like antimicrobial peptides.

Overall funding for STI R&D has more than doubled since we began collecting data in 2018, rising from $96m to $217m. A near-tenfold increase in industry funding accounts for most of the net growth. The Gates Foundation – which began its (non-HIV) STI funding only in 2021 alongside the establishment of its Women’s Health Innovation Team – providing another $11m. This overall growth partly reflects the growing burden of some STIs in high income countries, and comes amid the backdrop of growing concerns about the rise of antimicrobial resistance in STIs. Gonorrhoea, in particular, has been identified by the WHO as a priority AMR risk and accounts for 30% of the long-term growth in STI R&D.

The largest area of growth in STI funding in 2023 was funding for herpes simplex virus 2 (HSV) R&D, which rebounded from a slight drop in 2022 to reach $84m in 2023. However nearly half this growth in 2023 was from a new survey participant that year for a project which likely began a year or two earlier – and for which we do not have historical data. So while our long term growth estimate – $66m or 364% since 2018 – is likely accurate, the 2023 increase is a little overstated.

HSV-2 has gone from receiving less than 20% of STI funding in 2018 and 2019 to almost 40% in 2023. This is largely a result of growing industry funding for vaccines and especially biologics – mostly therapeutic vaccines – reflecting their huge commercial potential, particularly in HICs. Private sector funding for HSV-2 rose from $11m in 2018 to more than $76m, leaving industry responsible for 90% of the 2023 total. Funding from the US NIH, the only other major contributor to HSV-2, has remained relatively stable at around $8m. Like industry, the NIH focused on vaccines, including a new $0.8m grant in 2023 for early-stage mRNA vaccine development.

Mirroring the overall trend for STIs, funding for gonorrhoea dipped slightly in 2022 (down $9.4m, -14%) before rebounding strongly in 2023. Both the rise and fall were due to a temporary lull in industry’s vaccine funding (down by $5.7m in 2022 from the previous year's record high) and large cyclical shifts in funding from CARB-X – a global nonprofit pooled funding partnership for AMR-related R&D. CARB-X provided several large, up-front disbursements for drug R&D – totalling $14m – in 2019, before shifting its focus to vaccines in 2023, along with a significant amount of AMR gonorrhoea-relevant multi-STI diagnostic funding covered under ‘multiple STIs’, below.

While funding from both industry and CARB-X returned to around 2021 levels in 2023, the record high in gonorrhoea funding was driven by $7m for basic research from the Gates Foundation. This was its first ever reported contribution to gonorrhoea R&D, and went towards an epidemiological proof-of-concept study on gonorrhoea vaccine uptake among adolescent girls and young women in South Africa.

Despite the Gates Foundations’ boost to basic research, most gonorrhoea funding in 2023 still went to preventive vaccines, as was the case in each of the previous three years. Around half the 2023 vaccine funding, and a similar share of the rapid growth since 2018, came from industry, which focused its gonorrhoea investment exclusively on vaccine R&D. Much of the remaining funding for gonorrhoea R&D was provided by the NIH, which – despite a drop in its vaccine funding – maintained its position as the largest overall funder of gonorrhoea R&D.

Funding for chlamydia remained mostly unchanged at $28m in 2023, although this was up more than $16m (145%) from its 2018 level following rapid growth in the years leading up to 2022. The majority of the funding in 2023, and most of the growth since 2018, came from either the NIH (with $15m in 2023 funding, up $4.3m from 2018) or industry ($11m, up from nothing in 2018), with NIH funding focusing on basic research and industry on vaccines. After earlier falls in diagnostics funding from the NIH and the German BMBF, this left overall funding in 2023, as in each of the three previous years, split relatively evenly between basic research and vaccines.

The third largest contributor to chlamydia R&D in both 2022 and 2023 was the Indian ICMR – which was also the only substantial LMIC contribution to STI R&D. Funding from the ICMR averaged a little under $1.2m a year since 2021, when it began. This was more than ten times the total from the next largest funder – the Canadian CIHR – underlining how little interest there remains in chlamydia R&D outside the NIH and industry.

Funding for syphilis declined by 21% ($2.5m) from 2022's record high to $9.4m – or less than 5% of overall STI R&D. Even after this decline, though, 2023 syphilis funding was still more than four times its 2018 total.

Both the 2022 rise and the 2023 fall were mostly due to a much-needed spike in early-stage vaccine funding from Open Philanthropy, which left it responsible for two-fifths of global syphilis R&D in 2022. The decline in Open Philanthropy’s 2023 funding was partly offset by a rebound in contributions from the NIH and further growth in funding from the Gates Foundation. These three organisations – Open Philanthropy, Gates and the NIH – have driven the overall growth in syphilis funding, increasing from just $2.2m in 2018 (at that time all of which was from the NIH), to a combined $8.7m in 2023. This included a record $3.6m from the NIH, for mostly vaccine-oriented basic research.

Human T-lymphotropic virus 1 (HTLV) is the only individual STI to have seen its funding decline since 2018, dropping a further $0.9m to $6.0m in 2023. This long-term decline is essentially all due to reduced basic research funding from the NIH, which has dropped by 41% ($3.4m) since 2018. Both the 2023 drop and the long-term fall were exacerbated by a 2023 cessation in funding from Wellcome, which had provided at least half a million dollars each year prior to 2023, mostly for basic research.

These declines contributed to a $0.5m drop in basic research, to a record low $4.8m. Despite this, basic research continued to account for more than 70% of overall funding, as it has every year, as researchers attempt to find out more about the virus’ little-understood pathology and epidemiology. The only area with meaningful long-term growth has been HTLV vaccine R&D, which rose from less than $18k in 2018 to $0.9m in 2023 thanks to new funding from the NIH. Though the amounts remain small, the $2.5m spent on HTLV vaccines over the previous three years represents nearly forty times the total over the first three years of the survey.

The Japan Society for the Promotion of Science, whose funding reflects the unusually high prevalence of HTLV in Japan, has provided an average of $0.2m a year since 2018, and was the only supporter of HTLV vaccine R&D until the NIH began providing funding in 2021.

Funding for R&D addressing multiple STIs was mostly unchanged at $12m in 2023, down by just under $2.4m (-16%) from its 2018 level. A long-term downward trend partly reflects a highly variable stream of lump-sum diagnostics funding from CARB-X, much of it coming in 2020 following a call for proposals for diagnostics targeting gonorrhoea alongside other STIs. CARB-X funding will likely prove to have rebounded sharply in 2024 after it launched another call for gonorrhoea products, including $1.8m for a recently approved at-home test for chlamydia, gonorrhoea and trichomoniasis.

Multiple STI funding from industry, which has focused exclusively on diagnostics, has gradually grown from nothing at all between 2018 and 2020 to $6.5m in 2023 – leaving industry as the largest funder in a down year for CARB-X. Meanwhile, contributions from the NIH – especially for diagnostics – have trended downwards, falling by two-thirds ($3.9m) since 2018.

Overall multiple STI R&D funding remains focused on diagnostics, which received more than three-quarters of 2023 funding and a little over two-thirds over the life of the survey. This reflects the global need for and prioritisation of products which can be used to diagnose multiple STIs in a single application, especially in low-resource settings.

Funding for the Other STIs category, which includes AMR-risk STIs such as trichomoniasis and M. genitalium, narrowly surpassed its previous 2021 high of $4.1m to reach a peak of $4.3m in 2023, still just 2% of STI spending. Funding for basic research plays a key role in these often poorly understood diseases, and jumped to $2.4m (up $2.2m, 1270%) thanks to the US NIH and the Gates Foundation. Industry did not provide any funding in 2023, after contributing a total of $2.8m for M. genitalium diagnostics between 2021 and 2022.

Human papillomavirus (HPV) is the leading cause of cervical cancer, contributing to the approximately 660,000 new cases and 350,000 cervical cancer deaths each year, with its highest rates of incidence and mortality in LMICs. Vaccination is an effective tool for preventing HPV, but accessibility issues in LMICs remain, due to cost, multiple dose regimens and cold-chain storage requirements. Low-tech diagnostic tools could improve early detection and treatment, and novel therapeutic antivirals and medicines are needed for individuals already exposed to HPV, since most sexually active men and women will acquire at least one genital HPV infection during their lives.

Funding for human papillomavirus & HPV-related cervical cancer (collectively referred to here as just ‘HPV’) partly rebounded in 2023 after a sharp drop in 2022, rising by $13m (11%) to $125m. This left it $17m below its 2021 peak but up $25m (25%) over the life of the survey.

The growth since 2018 mostly reflects contributions from the top two funders: the NIH and industry. NIH funding has grown by 37% ($13m) since 2018, to a total of $47m – or nearly 38% of overall funding. Funding from the NIH focused heavily on basic research, accounting for nearly 80% of HPV basic research since the survey began. Industry's funding was up $17m (65%) since 2018 and focused increasingly on vaccines. Industry has seen its spending on vaccine R&D rise more than sixfold since 2018, to $39m, mostly on novel candidates rather than dose reduction studies for existing products, which had previously been the focus of HPV vaccine R&D. This growth has left industry responsible for substantially more than half of HPV vaccine R&D, though this may soon change following the mid-2024 abandonment of one major candidate following unimpressive trial results.

In 2023, we also saw a record $2.4m in HPV funding from the Indian ICMR – exceeding its total funding over the previous five years put together.

Nearly 40% of HPV funding was for clinical development & post registration studies, three-quarters of which was for vaccine trials. This funding is predominantly for post-registration, dose reduction studies of existing HPV vaccines over advanced clinical development of new vaccine candidates moving through the pipeline. There is still significant interest in dose reduction trials, with some recent successes demonstrating equal efficacy, and paving the way towards reducing barriers to uptake in LMICs where multi-dose regimens can be challenging to complete.

Figure 3 – funding for sexually transmitted infections including HPV

*Includes STIs with AMR risk only

Contraception, multipurpose prevention technologies and abortion

Funding for all three areas saw either low or declining funding in 2023

Despite the availability of various contraceptives, 218 million women have an unmet need for contraception globally, contributing to 111 million unintended pregnancies each year. Meeting women’s and men’s need for modern contraception would lead to unintended pregnancies dropping dramatically – to 35 million – with 21 million fewer unplanned births and 26 million fewer unsafe abortions annually. Current contraceptive use is hindered by real or perceived side-effects, as well as accessibility issues in low-resource contexts, where the need for administration by a skilled health professional (for example for IUDs) and short shelf lives can pose barriers. Because contraceptive efficacy depends on methods fitting users’ preferences, contraceptive R&D should respond to growing demands for user-controlled, on demand, non-hormonal options, as well as innovative contraceptives for men.

Funding for contraception R&D dropped to its lowest ever level in 2023, down $20m (-16%) to $107m, having fallen every year since 2019. It is now down a total of $51m, or almost a third, from its 2019 peak.

The 2023 drop was mostly due to a $17m (-25%) reduction in funding from the Gates Foundation, which returned to roughly its normal levels after spiking by $14m in 2022. The longer-term reduction, though, is largely the result of decreased funding from industry (down $38m, -69% from its 2019 peak).

Almost all of this 2023 decline fell on long-acting reversible contraception (LARC, down $19m, 47% to $21m), which has also borne the brunt of the longer-term decline (down $45m, -68% since 2019). Falling LARC R&D reflects ongoing reductions in industry funding (now down by 84%), alongside the return of Gates LARC funding to around normal levels in 2023 after two years of increased spending in 2021/22 focused on supporting Dare Bioscience’s early-stage development of a novel long-acting, user-controlled hormonal contraceptive implant. These falls have taken the share of contraceptive R&D funding going to LARC from 42% in 2019 to less than 20% in 2023.

This shift away from long-acting contraceptive research has been accompanied by an apparent move towards user-controlled technology – though a rise in funding which does not specify user control makes it hard to be completely sure. Looking only at products which do specify control, the share of funding for user-controlled products has risen every year, from 26% in 2018, to 70% in 2023. Partly, this is just the effect of the same decline in industry funding that drove the reduction in LARC funding, since industry’s spending was mostly on long-acting, non-user-controlled devices. But even excluding this, user-controlled funding has risen from a little over half the 2018 total to 80% in 2023 – suggesting a meaningful shift towards user-centred design of products in line with increasing recognition of autonomy and convenience as key to successful adoption. The growing category of user-controlled product development includes a record $1.9m in funding from the Male Contraceptive Initiative for a range of projects, including $0.5m for the YourChoice male contraceptive pill, which recently progressed to Phase I trials.

Despite some growth in male contraceptive R&D, contraceptives targeting female end users continued to dominate, accounting for almost three-quarters of total funding. R&D targeting male end users did rise, to a record 17% of the total in 2023, up from just 9% in 2018. These mostly focused on short acting methods (two-thirds of total male contraceptive funding), including multiple late-stage grants from the NIH for the evaluation of NES/T gel – a combination of Nestorone and testosterone.

Multipurpose prevention technologies are interventions that offer concurrent protection against pregnancy, HIV and/or other STIs in a single product, typically relying on one or more drugs, biologics, microbicides or devices. By combining prevention methods into products designed for (largely) user-controlled administration, MPTs offer the potential to streamline and democratise preventive healthcare, reduce health provider visits and put options in the hands of those who need them. While dual protection is of interest in any context, MPTs might be particularly useful in LMICs, where addressing multiple indications at once, in a convenient user-centric package, would help to address compounded health risks in particular populations and regions. Long-acting delivery systems such as subdermal implants, vaginal rings, and injectable formulations, as well as on-demand gels, fast-dissolving inserts and pills have shown promise in studies. However, most remain at the early stages of development.

Funding for multipurpose prevention technologies (MPTs) peaked in 2018 when we first began collecting data and decreased in both 2022 and 2023, falling from nearly $60m in 2021 to just $29m in 2023, its lowest ever level of funding.

Both the 2018 and 2021 peaks, and the subsequent declines were the result of changes in industry’s microbicide funding, the latter following failed product trials. Despite a partial rebound in 2021, industry funding has now fallen by more than 99% from its peak of nearly $46m in 2018, to just $28k in 2023 after the failure of a leading industry candidate.

In industry’s absence, the US NIH has become the dominant funder, responsible for a little over half of the non-industry total. USAID provided most of the remaining funding – a total of $34m over six years – making it the only other funder to invest more than $10m (total) in MPT R&D. As things stand, after the dismantling of USAID, none of this funding is slated to continue past 2025, further reducing the already critically small number of significant investors in MPT R&D.

In 2022 and 2023, around a third of contraceptive MPT funding was invested in devices and device/drug combinations – mostly intravaginal rings – leaving it as the largest product area following the drop in industry’s microbicide funding.

Biologics funding grew from nothing to $1.6m in 2022 and then doubled in 2023 to $3.3m – by far its highest level of funding ever. This sharp growth in biologics-based MPTs was mainly thanks to new US NIH funding for antibody-based contraceptive MPTs which leverage monoclonal human contraceptive antibodies (HCAs) – naturally occurring antibodies with strong sperm-agglutinating and -immobilising activity.

In contrast to contraceptive R&D, funding for MPTs which are non-hormonal and user-controlled have both fallen, with both categories down by more than $40m since 2018. This doesn’t seem to reflect the intended role of MPTs, and is in fact mostly due to a handful of investment drops from industry funding for microbicides (typically both non-hormonal and user-controlled) rather than a deliberate shift in priorities. Funding for hormonal products is basically unchanged since 2018, while there has been substantial growth in non-user-controlled options, mostly Gates- and NIH-backed multi-purpose implants and injectables. Funding across all product areas also remained exclusively for female targeted products, with zero reported funding for R&D targeting male-focused MPTs to date.

With such a small pipeline of products in development (only 21 as of 2025 and just five in clinical trials), and without ongoing USAID funding, and potential further reductions in US government funding, this area of research is now seriously under threat, and an absence of new products likely to continue.

Abortion is a common part of women’s reproductive lives regardless of the legal context in which they live. When properly administered, it is one of the safest medical procedures available, but nearly half of all abortions are unsafe, with potentially severe complications such as life-threatening blood loss, infection, organ damage, and death (5-13% of maternal deaths annually). Research and development into additional drug regimens, very early abortion (menstrual regulation) products and higher sensitivity early pregnancy tests could contribute to improving accessibility of safe abortion and reduce the global burden of unsafe procedures.

Abortion received just $1.1m in R&D funding, all for drug R&D.

Almost all of this funding (99.8%) came from Grand Challenges Canada, with the remaining 0.2% coming from industry (just $2k) for early menstrual induction drugs – funding which we know has been ongoing at a similarly low level since 2019, prior to the inclusion of abortion R&D in the G-FINDER survey.

This was the lowest total of any of the areas included in this report, probably due partly to the politicised environment of abortion in general, and a possible perceived lack of R&D opportunity. It is dismally low nonetheless.

Figure 4 – funding for contraception, MPTs and abortion

MPTs

Contraception

Abortion

Gynaecological conditions

Funding for gynaecological conditions is dominated by US NIH-funded basic research

This category includes conditions which are specific to women’s health but not those directly related to maternal health, which are covered immediately below. The included conditions – uterine fibroids, polycystic ovary syndrome (PCOS), endometriosis and menopause – were all introduced in the survey for the first time in 2023.

Menopause, typically occurring between ages 45-55, marks the end of a woman’s reproductive years and can cause hot flashes, night sweats, sleep disturbances, mood changes, vaginal dryness, joint pain, and cognitive symptoms. It is also associated with an increased risk of cardiovascular disease, osteoporosis (where bones become weak and brittle), and stroke, and may cause changes in weight distribution, decreased bone density, and urinary issues. Research-driven advancements in menopause care are needed to improve the quality of life and health outcomes of women negatively impacted by their menopausal and perimenopausal symptoms, alongside better diagnostics to personalise treatment plans. Current options focus on hormonal therapy, which is safe and effective, but it is contraindicated for women with a history of hormone-sensitive cancers and its high cost limits its applicability in LMICs. Basic research to improve the understanding of menopause risks for cardiovascular, cognitive, and musculoskeletal health as well as new non-hormonal therapeutics are needed to improve clinical management and outcomes.

Menopause received $28m in 2023 R&D funding, representing (narrowly) the largest recipient among the gynaecological conditions. Most menopause funding was allocated to either drug development ($8.6m, 30%) or basic research ($16.5m, 58%), the latter reflecting growing interest in better understanding the condition and its symptoms.

The US NIH was the primary funder, contributing 85% of the total. Mirroring the overall distribution of funding, most of this was directed towards basic research ($15m, 64%), and drugs ($7.9m, 33%), targeting a range of menopause-related conditions including perimenopausal mood disorders and Alzheimer’s prevention. Most of the remaining funding was in the form of industry’s clinical development of intravaginal hormone rings ($2.3m, 8% of the total).

Endometriosis is a chronic, estrogen-dependent condition that causes endometrial-like tissue to grow outside of the uterus, estimated to affect about 10% of women globally. Commonly affecting organs such as the ovaries, bladder, and bowel, it leads to debilitating symptoms such as chronic pelvic pain, painful periods, and infertility, with over 60% of women with endometriosis experiencing persistent pain. The aetiology of the disease is poorly understood as a result of the historical neglect of gynaecological conditions in medical research, and both diagnostic and treatment options are very limited. Diagnosis can take years due to the lack of non-invasive options, with definitive diagnosis ultimately requiring surgery. There is no cure for endometriosis and treatment is limited to symptomatic management with repurposed medicines (pain medications and hormonal medicines) which have limited efficacy and do not address the cause of the disease nor alter its progression. Basic research to improve our understanding of the pathology is urgently needed, as well as more accessible diagnostics and targeted medicine development.

Global funding for endometriosis also totalled $28m in 2023 – far below the R&D funding received by other conditions with similar prevalence, as outlined in our recent report on women’s pain. Over half of all endometriosis R&D funding in 2023 was for basic research ($17m, 59%), again reflecting an emerging interest in filling knowledge gaps on the basic pathology of the disease. Drugs received the next largest share ($6.5m, 23%), including $0.6m from the NIH for the use of heated nanoparticles to destroy lesions. Despite the urgent need for diagnostics beyond laparoscopic surgery, just 11% ($3.2m) of funding was dedicated to diagnostic development.

Apart from a small grant ($0.02m) from the Society for the Advancement of Gynecologic Excellence, a Canadian philanthropic organisation, all endometriosis funding came from the public sector, with 90% of all funding originating from the US NIH ($25m). Contributions from the eight other funders lagged far behind, headlined by the European Commission’s $1.1m (4% of total funding, for diagnostic development), the French National Research Agency ($0.7m, 2%, for basic research) and the Australian National Health and Medical Research Council ($0.4m, 2%, for basic research and drug development).

With funding coming mostly from high-income country research organisations – as they begin to acknowledge the scale of endometriosis’s burden following high profile advocacy in this area – two LMICs also funded research for endometriosis: the Argentinian National Council for Scientific and Technical Research (CONICET) contributed $20k, and the Indian Department of Biotechnology, Ministry of Science and Technology (DBT) contributed $200k.

Just 7% ($1.9m) of endometriosis funding went specifically to clinical development, all of it from the NIH for drug trials, suggesting there will be a long wait for approved products.

Uterine fibroids are common fibrous or muscular growths of the uterus, with a, estimated prevalence of between 45 and 69%, with the highest rates seen in women of African descent. Fibroids can cause pelvic pain (20-40% of cases), abnormal uterine bleeding, urinary problems, infertility and pregnancy-related complications. Their aetiology is poorly understood, which translates to a limited range of options for diagnosis and treatment: diagnosis is typically achieved through ultrasound or MRI and current treatment options include anti-inflammatory drugs for pain and bleeding management and hormone therapy or surgery, albeit with limited efficacy. Many of these options are costly and inaccessible in low-resource settings. Research and development needs for uterine fibroids are wide-ranging: basic research to better understand the pathology would be a starting point to any targeted product development while more accessible diagnostic options are needed especially in LMICS. An improved understanding of the condition, alongside targeted treatments (ranging beyond surgery and repurposed hormonal drugs) which can prevent fibroids growth or decrease their size, have the potential to significantly improve women’s quality of life and lower the global burden of this condition.

Funding for uterine fibroids totalled $12m in 2023. As with most other gynaecological conditions, the vast majority of this funding was for basic research ($11m, 86%) reflecting the difficulties presented for product development by the lack of a thorough understanding of these conditions. Drugs received the next largest share ($1.7m, 14%), while diagnostics accounted for only 1% of the total funding ($0.1m).

Of the $1.8m devoted to product development for uterine fibroids a little under half was US NIH support for post-registration studies of the drug letrozole, which can shrink fibroids by reducing estrogen production within the fibroid cells. Almost all the remainder went to a Phase II study on fertility improvement with epigallocatechin gallate (EGCG) , also entirely funded by the NIH. The small amount of funding for diagnostics came from a combined grant exploring the use of stress strain ultrasound imaging for the detection and characterization of endometriosis and uterine fibroids.

The NIH was responsible for essentially all the global funding for uterine fibroid R&D in 2023 (99.7%), the sole exception being a small grant ($40k, 0.3%) from the UK Medical Research Council for basic research.

Polycystic ovary syndrome (PCOS) is a complex hormonal disorder affecting around 20% of women globally with a range of clinical manifestations impacting metabolism, ovarian function and hormonal balance. Despite its high prevalence, PCOS remains poorly understood: diagnosis is based on a complex set of criteria requiring imaging and laboratory testing, with limited accessibility in low-resource settings. Treatment is limited to symptomatic management using repurposed therapeutics to address hormonal, metabolic and fertility-related symptoms, with no cure or medicine addressing the underlying cause. Basic research, diagnostic development for point-of-care and affordable testing, and novel therapies targeting the cause of the syndrome and offering more efficient management of its symptoms are needed to alleviate the burden of this disease globally.

Funding for polycystic ovary syndrome (PCOS) totalled $9.7m in 2023. As elsewhere, around three quarters of all PCOS funding in 2023 was for basic research ($7.2m, 74%). The second largest share went to diagnostics ($1.3m, 14%), followed by drugs ($0.8m, 8%).

Only 6% ($0.5m) of funding was for clinical development, all of it for an NIH-funded Phase III trial of semaglutide – the well-known diabetes and weight loss drug which shows promise in treating the weight gain and metabolic syndrome caused by PCOS. The NIH provided 86% of funding overall, and almost all of the funding for product development, with the only exceptions being $0.2m for a preclinical study on 17beta-Hydroxysteroid Dehydrogenase inhibitors from the Indian ICMR and $9k for early-stage diagnostics from the Indian BIRAC.

Alongside the NIH, three Indian public funders – ICMR, BIRAC and the DBT – provided just over 6% of total funding ($0.6m) between them, leaving PCOS with the largest LMIC funding share of any individual SRH condition. Wellcome accounted for most of the remainder provided a further $0.6m (6.3% of the total) for basic research on androgen excess and metabolism.

Figure 5 – funding for gynaecological conditions

Menopause

Uterine fibroids

Polycystic ovary syndrome (PCOS)

Maternal health conditions

Preeclampsia funding reaches a record high; while PPH falls back to 2018 levels

This category covers four maternal health conditions: postpartum haemorrhage (PPH), preeclampsia and eclampsia (PE&E), preterm labour, and maternal iron deficiency anaemia. The last two were added to the survey this year and have only a single year of funding data.

Preeclampsia is a pregnancy-related disorder of the placenta and its blood vessels, and is characterised by sustained high blood pressure, protein in the urine, and/or organ complications after 20 weeks' gestation. It is a leading cause of maternal death (16%), stillbirth, and early neonatal mortality (10%) worldwide. Due to its historical neglect in medical research and the complexity of such a multifaceted disease, diagnostic and treatment options remain limited. Early detection and prediction of preeclampsia would be critical to improve clinical management and prophylaxis (aspirin) but despite a dynamic biomarker research space, current testing tools have limited diagnostic performance. Currently only one medicine exists once the disease manifests clinically – magnesium sulphate – and only to prevent and treat seizures associated with severe preeclampsia/eclampsia. The only truly curative treatments remain early delivery or termination. There is a need for better options, both for safer symptomatic relief medications, and for new therapies that target the underlying pathophysiology of the disease rather than off-label use of drugs with limited safety and efficacy.

Funding for preeclampsia & eclampsia (PE&E) totalled $178m in the five years from 2018 to 2023, with 2023’s total of $40m representing a 108% increase from 2022 and (narrowly) a record high. The $21m rebound in 2023 left total funding more than $20m above its 2018 level.

Historically, fluctuations in PE&E funding mostly reflected changes in the contributions from the US NIH, which was the largest single funder every year, with a strong focus on basic research – which continues to receive more funding than any other product area. Funding from the NIH rebounded to $21m in 2023, following a big fall in 2022. The cause of the record high in 2023, though, was a surge in funding from the Gates Foundation. It has gradually increased its PE&E funding from $0.6m in 2018 to more than $11m in 2023, with big increases for diagnostic and drug funding, including $2.1m to the Concept Foundation for the largest ever trial on use of low dose aspirin, aimed at determining optimal dosage.

This increase in overall Gates Foundation funding represents about half of the net growth in funding in 2023 and about half of the $20m in overall increase since 2018. The previous spike in PE&E funding, in 2019, resulted from $12m in (ultimately unsuccessful) biologics funding a small pharmaceutical company. Despite some evidence of industry activity in the product pipeline, there has been no reported industry investment from survey participants since 2020.

Postpartum haemorrhage (PPH) is the leading cause of maternal death globally, affecting approximately 14 million women annually and resulting in around 70,000 deaths each year. PPH is defined by blood loss exceeding 500ml after birth. Most cases are caused by either: lack of muscle tone or contractions (‘atony’) in the uterus following delivery (70% of cases); trauma, such as genital tract lacerations; part or all of the placenta remaining in the uterus after childbirth; or impaired blood clotting (‘coagulopathy’). In high-income countries, most births occur in places where drugs to help uterine contraction (uterotonics) and surgical interventions are widely accessible, contributing to generally low rates of maternal death from PPH. However, while medicines are the cornerstone of PPH prevention and treatment, the current catalogue is suboptimal, particularly for LMIC settings where issues related to quality, cold-chain transport and storage, and skilled administration limit access. Heat-stable and easy to administer (inhalable or sublingual) medicines are needed to provide access in low-resource settings. Low-tech bleeding-control devices can be an alternative when medicines fail or are unavailable, but more evidence of their efficacy, as well as wider distribution, are needed to maximise their impact.

Global funding for postpartum haemorrhage (PPH) rebounded to a record $11m in 2022 before declining by 21% to $8.6m in 2023.

Falls in PPH funding after 2018 were the result of declining industry funding, which fell from over $7m in 2018 to just $0.8m in 2021 before rebounding a little in 2022. With industry funding declining again in 2023 following the successful completion of African heat-stable carbetocin trials, the rebound in overall PPH funding was instead driven by a new line of drug funding from Unitaid that began in 2022. Unitaid provided more than $6m in both 2022 and 2023, mostly for the Accelerating Measurable Progress and Leveraging Investments for Postpartum Haemorrhage Impact (AMPLI-PPHI) implementation trial, which aims to demonstrate the relative feasibility and cost-effectiveness of heat-stable carbetocin, tranexamic acid, and misoprostol in various LMIC settings.

The other major factor in PPH funding’s rebound from its record low in 2021 was the 2022 commencement of funding from the US NIH. It contributed a total of $1.6m over the last two years, for a mix of drug and device R&D, the latter representing the first definitive randomised controlled multicentre trial of the FDA-approved ‘Jada system’ in Ghana, gathering critical data on its effectiveness, safety and cost effectiveness at treating PPH.

Drug R&D continues to account for the vast majority of PPH funding: 89% of the 2023 total and over the life of the survey, with the remaining 11% going to devices and device/drug combinations– in contrast to most other areas of maternal health, funding for basic research into PPH is not included in our survey since the physiology of the condition is well understood.

Preterm labour – defined as the onset of childbirth before 37 weeks – is one of the leading causes of neonatal mortality worldwide, responsible for around 900,000 neonatal deaths each year. Both neonatal mortality and morbidity rates are higher in LMICs, due to limited access to neonatal care. Despite the substantial burden of preterm birth, current treatments rely on tocolytics (medicines that delay preterm labour by relaxing uterine contractions), despite their limited effectiveness and often significant side-effects and risks for maternal and neonatal health. A lack of understanding of this multi-causal condition has historically hindered the development of therapeutics addressing the causes of preterm labour. Basic research and biomarker diagnostic research, by uncovering pathological pathways, have the potential to improve the medical understanding of preterm labour, screening capabilities and ultimately therapeutic interventions and preventive strategies to reduce its global burden. Promising approaches include medicines targeting various stages of the known inflammatory cascade associated with preterm labour, such as interleukin-1 receptor (IL-1) inhibitors and cytokine suppressive anti-inflammatory drugs.

Global funding for preterm labour R&D totalled $35 million in 2023. The majority of funding went to basic research ($27m, 77%), as we grapple with an emerging understanding of the complexities of the underlying causes of the condition. Remaining funding was mostly divided between drugs ($4.9m, 14%) and diagnostics ($2.4m, 7%). Funding for biologics was just $0.6m, with only $17k devoted to dietary supplement R&D – an area included in the G-FINDER scope only in relation to preterm labour and iron deficiency anaemia (below), where there is ongoing research targeting novel products or formulations – in the case of preterm labour mostly looking at animal modelling of the potential role for the amnio acid L-arginine in preventing brain damage from preterm birth.

More than 90% of overall funding was provided by the US NIH, a total of $32m which included 99% of funding for drugs and 95% of basic research spending, the latter mostly focused on understanding the aetiology of preterm labour and the role of the vaginal microbiome in the early onset of labour. The NIH was also the biggest funder of diagnostics ($1.0m, 43% of the total) and biologics ($0.4m, 71%).

The EC was the second biggest contributor, providing a total of $1.0m for late-stage diagnostic funding for Fine Birth, the first non-invasive point-of-care device designed to predict the risk of preterm labour in real time.

Maternal iron-deficiency anaemia is a significant global health concern affecting approximately 37% of pregnant women worldwide, and a significant risk factor for maternal mortality, with around 20% of maternal deaths potentially stemming from this condition. Prevalence increases up to four-fold in LMICs due to dietary deficiencies, gut conditions, and an increased risk of infections and inflammation that inhibit iron absorption. Iron supplementation is the primary course of treatment, but its effectiveness varies depending on the formulation and oral iron is often poorly absorbed and can cause side effects such as gastrointestinal discomfort, nausea, and constipation, leading to high rates of discontinuation. Affordable point-of-care diagnostics would improve the identification of the type of anaemia and alternatives to oral or IV iron are needed to decrease the global burden of this condition on pregnant women and their infants.

Maternal iron deficiency anaemia (IDA) funding totalled just $2.8m in 2023, and was provided by just two funders. The US NIH provided the vast majority of global funding ($2.4m, 86% of the total) with the remainder coming from the Australian NHMRC ($0.4m, 14%), leaving IDA with the second lowest funding total of all the conditions included in the survey (only abortion received less). There was no reported maternal IDA funding at all from the private or philanthropic sectors. This absence is probably partly due to the wide range of iron supplements already on the market and the resulting lack of commercial interest in developing new and better ones; but also partly due to the G-FINDER survey’s currently limited coverage of the dietary supplement industry.

The largest single share of reported maternal IDA funding went to drug R&D, which totalled just over $1m (37% of the total), including all $0.4m from the Australian NHMRC.

Remaining funding – all of it from the NIH – was relatively evenly split between basic research ($0.8m, 29%) and diagnostics ($0.7m, 25%), with just 9% ($0.2m) going to dietary supplements, for a study of the feasibility of oral lactoferrin to prevent iron deficiency anaemia in obese pregnant women.

Figure 6 – funding for maternal health conditions

Preeclampsia & eclampsia

Postpartum haemorrhage

Preterm labour

Maternal iron deficiency anaemia

R&D for more than one SRH issue

Non-issue-specific funding has increased every year since we began our survey and is now more than six times its 2018 total, mostly driven by platform funding

This section covers funding that cannot be allocated to a specific SRH condition. ‘Core funding’ refers to non-earmarked funding given to organisations that work on multiple areas, where the distribution of funding across diseases is not determined by the funder. ‘Platform technologies’ are tools that can be applied to a range of pathogens, but which are not yet focused on a particular disease or product. ‘Other R&D’ captures any remaining grants that cannot otherwise be allocated, including grants targeting multiple diseases.

Global R&D funding targeting more than one SRH issue (‘non-issue-specific’, or ‘NIS’ funding) maintained its upward trend, growing more than sixfold from its 2018 level to hit a record $202m in 2023. This increase has been driven largely by steady growth in funding for SRH-applicable platform technologies, which account for almost 70% of NIS funding. As with overall NIS spending, platform funding has risen more than sixfold since 2018, reaching a total of $170m in 2023.

Remaining NIS funding was divided between SRH-relevant core funding to multi-disease organisations like the Barcelona Institute for Global Health ($43m, 18% of the 2023 total – and up $12m from 2022), core funding of SRH R&D organisations ($11m, 4%, up by $1.6m) and a range of hard-to-categorise ‘Other R&D’ ($21m, 9%, up $8.2m).

Funding for SRH-applicable platform technologies grew for the fifth year in a row, reaching an all-time high of $139m in 2023, with much of the funding seeming to be primarily intended for use against emerging infectious diseases. Almost half of this funding in 2023 went to vaccine related platform technologies ($79m, 46%) with most of the remainder split relatively evenly between drug-related platforms ($24m, 14%), adjuvants & immunomodulators ($27m, 16%), and general diagnostic platforms ($31m, 18%). Biologics-related platforms received the remaining $9m – just 5% of total platform funding.

The Gates Foundation continued to dominate the platform funding landscape, following a modest increase in 2023 (up $25m, 34%). This left the Foundation responsible for more than half of 2023’s SRH-relevant platform technology funding ($98m, 58%) with a strong focus on vaccine platforms, which accounted for almost two-thirds of its platform funding.

We consider the significance of rising platform funding for women’s health later in the report.

Core funding specifically for SRH R&D organisations totalled $11m in 2023, following a marginal increase from previous year (up $1.6m, 17%). This was the second year of funding growth and was attributable to two funders: the Indian ICMR, which provided $7.9m in self-funding; and the US NIH, which provided a record $3.0m.

Core funding to multi-disease organisations rose by 38% to $43m (up $12m), up fourfold from 2020’s record low. This growth mostly reflects a new line of funding, beginning in 2022, from the Czech Republic Ministry of Education to the Czech Institute of Organic Chemistry and Biochemistry which totalled $35m in the two years since it began, all of which is relevant to, but not intended for, SRH conditions.

Funding for SRH-related ‘Other R&D’ rose by 65% ($8.2m) in 2023 to reach $21m, after three years of relative stasis, thanks to increased contributions from the two largest funders: the Gates Foundation (up $4.3m, 206%) and the US NIH (up $1.8m, 41%). The EC also contributed $0.7m for a home vaginal microbiome screening kit with potential applications to SRH indications. Wellcome provided its first ever funding for Other R&D in 2023, to University of Oxford to support LMIC-based SRH-related activities across several different areas.

Figure 7 – Non-issue-specific funding

Non-issue-specific

Discussion

New funding has focused on sexually transmitted infections, while contraceptive R&D has tumbled, as shifting private sector priorities have left a big gap in contraceptive product development

In our previous report on SRH funding, released in 2023, we expressed a concern that funding growth was largely the product of ‘spillovers’ from technologies intended for high-income countries or other areas of global health. We argued that: “It does matter that so much global funding focuses primarily on the needs of HICs. It distorts the distribution of funding away from maternal and pregnancy-related conditions, the burden of which is lower in HICs”

Since then, this skew has become more pronounced. Funding for sexually transmitted infections – including HPV – has now risen by a cumulative $147m since 2018, and by $70m in 2023 alone, with 80% of the long-term increase being provided by industry. This is, of course, good news. STIs are a huge problem in both high-income countries and, especially, LMICs; new ways to prevent, treat and detect them are a welcome response to the burden they impose, particularly on women, who disproportionately suffer from STIs. But we worry now, as we did then, that private sector investment is based mostly or entirely on the needs of high-income countries – and the commercial potential they imply. If and when these new technologies reach LMICs – where the STI burden is far higher, but commercial potential much lower – they will still have to be adapted to the specific needs of users and health systems, giving emerging resistant strains the chance to evolve, and then spread globally.

More concerning, though, is that the surge in funding for STIs has been accompanied by a rapid drop in funding – especially private sector funding – for contraceptive R&D. Total R&D funding for contraceptives and MPTs has fallen by $53m (-28%) since 2018, with half the drop coming in 2023 alone. Industry’s contraceptive funding is down even more sharply: by $83m, or 83%, to a little under $17m in 2023. Given the key role played by USAID and the NIH in funding these areas, recent cuts to US funding are likely to exacerbate this unwelcome trend.

This all suggests that whatever motivation existed for private sector investment in novel contraceptives when our survey began in 2018 has largely evaporated. Funders, especially pharmaceutical companies, are increasingly willing to tackle sexually transmitted infections, but none of the major industry players appear to have much interest in contraception, nor in MPTs.

Some of this may reflect the difficulty of valuing improvements in contraceptive technology – compared to those for STIs – under a traditional ‘health improvement’ framework. An unplanned or unwanted pregnancy is not a ‘disability’ in the Disability-Adjusted Life Year sense, nor just about improving health. So while providing women and men with safer and more convenient methods for securing reproductive autonomy is obviously valuable, and unplanned pregnancies economically costly, both are difficult for health systems to place a value on. The lack of interest in contraceptive and abortion R&D also reflects the practical and ethical difficulties associated with conducting medical research on ‘healthy’ populations, and the political sensitivities and litigious history that surrounds it.

Overall growth in sexual & reproductive health R&D has been driven by funding for platform technologies, which will need to be adapted to specific pathogens before they can make an impact

Funding for sexual & reproductive health R&D nearly doubled between 2018 and 2023, rising by $438m – or by $320m once we adjust for the new conditions we added this year.

Two things, though, prevent us from being as excited as this impressive rate of growth suggests we ought to be. The first is our caution over the private sector’s focus on HIC needs, and the impact it has on priorities and fitness for purpose of innovations for in LMIC contexts, which we discuss above. The second is that well over half of this growth comes from an increase in non-issue-specific (NIS) funding which is relevant to, but not intended for, the conditions included in our report.

The vast majority (almost 90%) of NIS funding came via grants which we considered relevant to all three of the global health areas we cover: neglected disease and emerging infectious disease alongside SRH/women’s health. This global health (rather than SRH-specific) funding included 95% of platform spending, 80% of core funding and 68% of Other R&D. After accounting for funding directed to either SRH and emerging infectious disease, or to SRH and neglected disease, only $13m (5%) of 2023 NIS funding was specifically directed to sexual & reproductive health – a figure that has remained largely unchanged since 2018. Funders are giving much more money to a range of (potentially) SRH-relevant technologies, which is wonderful, but many are doing so largely without intending to.

As with the rise in STI funding, growing NIS funding is in many ways good news: platform technologies like mRNA and ChAdOx helped us survive COVID, and have the potential to transform drug and vaccine development for STIs. But only “the potential”. And mostly only for STIs.

Our first concern, then, is that growth in funding for platforms almost exclusively intended for use against pathogens has exacerbated the concentration of SRH funding on research relevant only to STIs. If we include the $170m in platform funding, then almost four-fifths of 2023’s issue-specific funding was relevant just to STIs.

Our second note of caution is that platform technologies only help with STI product development if they are actually used to develop products for STIs. Much of the rapid growth in platform technology funding came after (and, we believe, as a result of) COVID, and seems heavily focused on the laudable goal of responding to future epidemics. Only one of these post-COVID technologies has, so far, been applied to STIs – an early-stage mRNA vaccine for HSV-2 under development at the University of Pennsylvania. So a rise in funding with the potential to improve sexual and reproductive health is welcome, but no substitute for the next stage of development which will be required to transform potential into impact.

Realistically, the platform technologies which account for an increasing share of what we label as ‘sexual & reproductive health R&D’ will not deliver new products for STIs in the near term. Instead, they capture investment in innovations that could pay off in the future. They will have a lower probability of success for each individual disease indication, but as we have seen with COVID, finding the right disease to which they can be applied can unlock their potential, provided we have laid the necessary foundations. This kind of moonshot innovation is vital, but no substitute for the hard (and costly) work of applying it to SRH, meaning that the sharp growth in funding should not necessarily be taken at face value – a dollar spent on vaccine platforms means something very different than a dollar spent on endometriosis, but our measure of total funding treats them as interchangeable.

Female-only conditions remain the most significant area of neglect, receiving only a small share of SRH funding

The extension of the scope to include additional maternal and gynaecological health conditions further highlights the consequences of gender bias in R&D funding: even within the relatively female-focused field of SRH, conditions that affect women exclusively receive a lot less funding than conditions affecting both women and men (STIs, HPV and even contraception). Investment in maternal and gynaecological health together represents less than a quarter of the total SRH funding.

This lack of funding reflects the sad reality that, historically, women's health issues have been dismissed as women’s hysteria; that many of these conditions were not even believed to actually be conditions, but rather just a normal part of being a woman; that women have been essentially considered small men since the dawn of medical research; and because we still live in an environment where men’s issues are prioritised over women’s. As a result of all of this, the further R&D gets away from issues that affect men, the less funding it receives. As we have previously argued:

On the global health stage, women’s health is equally deprioritised. Within LMIC-applicable R&D for sexual & reproductive health – arguably a women-centric health area to begin with – investment in conditions that exclusively affect women (maternal and gynaecological health) accounts for only 8% of the total, and represents only a small proportion of what is spent on other global health issues such as malaria (24%).

The high proportion of basic research funding, and small shares for clinical development, show how far we have left to go in developing product which address women’s health

R&D for sexually transmitted infections and contraception is based on relatively settled science that unlocks product development and, as a result, their funding is tilted heavily towards clinical development, which accounts for nearly half of funding for MPTs and HPV, and roughly a quarter of STI and contraceptive funding. This is much less true, though, of funding for the wider range of women’s health conditions included in this report. With the exception of well-understood areas like abortion and PPH, for which basic research is not included in our survey, funding for many of these conditions is heavily skewed towards the basic research needed to properly understand them, with very little funding directed to clinical development. Uterine fibroids, preterm labour and polycystic ovary syndrome all see more than 70% of their total funding go to basic research, with three more conditions – endometriosis, menopause and preeclampsia – spending over half their funding on basic research. Due in part to the heavy focus on basic research, these six conditions averaged only a little over $3m in 2023 clinical development funding, compared to more than $47m in HPV clinical development alone – albeit focused mostly on new regimens for existing vaccines.

Product development in many of these areas is made more challenging by the complex spectrum of conditions captured under a single label like ‘preeclampsia’. In many cases, women’s health conditions can present – and are experienced – very differently in different people, with the edge case being a condition like menopause, which all women experience but which can be pathological (to varying degrees and in varying ways) in a subset of cases.

Similarly, polycystic ovary syndrome is a complex disease that can look very different in different patients, with varying constellations of symptoms and often presenting similarly to other conditions, creating challenges for diagnosis and for the development of treatments that address its root causes rather than just its symptoms.

This level of variation within individual conditions presents an ongoing challenge to product developers, who in many cases may not even be able to identify the population their product is supposed to help. Addressing these barriers to product development through basic research is obviously a necessary first step, but leaves us furious that it is only happening now.

That we are only now beginning to wrestle with the complexity of these common conditions is a legacy of historical undervaluing, deprioritising and dismissing of women’s health, pain and wellbeing, and the reason that conditions with such high levels of incidence among women remain so poorly understood. Within this context, even a renewed (and welcome) energy and focus towards these conditions means that we are likely years away from a sufficient understanding of the basic science necessary for a robust pipeline of products addressing them – particularly in the face of cuts to funding from the NIH, the major sponsor of basic research in these areas.

Figure 8 – Proportion of R&D funding dedicated to basic research, for each condition, 2023

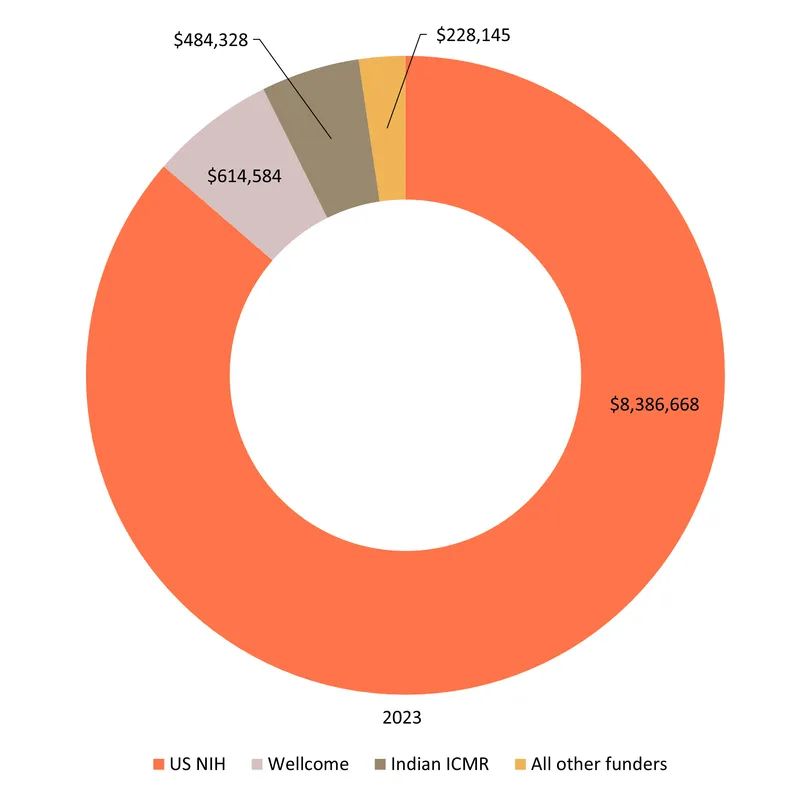

The US NIH, the Gates Foundation, and the pharmaceutical industry accounted for 82% of global SRH funding in 2023, and an even larger share of SRH-specific R&D

The NIH, the Gates Foundation and industry have been the top three sources of funding, in some order, every year since our survey began, with their share of global funding reaching a record 82% in 2023. As the chart below illustrates, industry now focuses heavily on STIs, the Gates Foundation on contraception and non-issue-specific funding – mostly platform technologies – and the NIH on almost everything, giving it a key role in several otherwise neglected areas.

The only substantial LMIC public funder was the Indian ICMR, which has seen its issue-specific funding grow every year since it began providing funding in 2019, from $0.4m to a record $5.0m in 2023 – most of it for HPV and other STIs. The ICMR ranks much higher – the sixth largest funder in 2023 – if we include its nearly $8m in 2023 non-issue specific self-funding, much of which went to the National Institute for Research in Reproductive Health in Mumbai.

As we have seen with the departure of industry leading to a sharp fall in contraceptive R&D, the growing dominance of these top three funders leaves SRH R&D increasingly vulnerable to a shift in their priorities, as we discuss below.

Figure 9 – Distribution of disbursements by funder and condition funded, 2023

The US government plays – or played – a critical role in funding SRH R&D: what happens next will have a big impact on the SRH R&D landscape going forward

In 2023, 40% of the world’s funding for sexual and reproductive health came from the US government. This was a record, but only narrowly: the US government’s share of global funding was 35% in 2022 and 2023, and just under 40% in 2021. Since our survey began in 2018, just over 37 cents in every dollar has been spent by the US government – with 99% of that total coming from either the US NIH (34% of global funding) or USAID (2%).

For many of the conditions included in our survey – menopause, PCOS, maternal iron deficiency, endometriosis, preterm labour, uterine fibroids – the NIH is responsible for more than four-fifths of their total funding and is often the only significant source of funding, as shown below:

Figure 10 – Number of major* funders vs share of funding provided by the US NIH, 2023

*Major funders are defined as those providing at least $1m, including the NIH where relevant.

Each year, we look at the massive share of R&D funding – for neglected diseases as well as SRH – attributable to the NIH and express both gratitude, and concern that we have allowed ourselves to grow so dependent on a single source of money. This year, with huge policy shifts within the US government and their near complete cessation of investment in global health and R&D, our ongoing worries have proved well founded. The dismantling of the US public health funding infrastructure has already brought a sudden halt to a number of SRH-related programmes. These include, for example, a USAID-funded CONRAD-led trial of novel long-acting contraceptives, and the CDC’s STI tracking programme, leaving their future, and the ability to salvage any meaningful data from long-running research efforts, in serious jeopardy.

We continue to believe that support for global health R&D is a global public good that delivers huge benefits to marginalised populations and that it generates economic benefits, employment and valuable intellectual property within the US itself. Based on our earlier research, America’s investment likely led to 600,000 new jobs, and $104 billion in economic activity within the US alone, to say nothing of the (more than $250bn) in benefits US-backed basic research will ultimately deliver to future scientists and everyone who benefits from their discoveries. And every dollar spent on global health R&D pays for itself more than 400 times over in averted death and disability across the world.

A focus on early-stage research and the impending departure of the US from its leadership role will lead to a massive shortfall in product development funding

As the figures above show, even prior to the changes in US government funding, product development for women’s health was frequently a shoestring operation, focused on (less costly) early-stage research and repurposing existing solutions for different problems.

Years of basic research, mostly supported by the NIH, have gradually led to an increased understanding of these long-neglected conditions and created the opportunity for funders to take the next step by actually investing in the products necessary to diagnose, prevent, treat and cure them.

Our survey shows a private sector that is increasingly focused only on sexually transmitted infections, and massive COVID-inspired investment in platform technologies that might one day revolutionise their treatment; but very little good news for contraception, gynaecological conditions or maternal health. There are now real opportunities to improve the lives of hundreds of millions of women but, instead, we now see even this limited progress under threat from the collapse in funding from the US government and the private sector.

If this new era of women’s health is to be more promising than the last, we need to see a change in heart from the funders who have until now avoided contributing to areas of R&D often seen as ‘too difficult’, or ‘political’, or simply not seen at all.

Sexually Transmitted Infections Pipeline

Explore the marketed products and pipeline candidates for sexually transmitted infections

Gynaecological Conditions Pipeline

Explore the marketed products and pipeline candidates for gynaecological conditions

Table of contents

- What this report tells us

- Sexual & reproductive and women’s health: A new era?

- What's in this report

- Overview of the funding landscape

- Sexually transmitted infections

- Contraception, multipurpose prevention technologies and abortion

- Gynaecological conditions

- Maternal health conditions

- R&D for more than one SRH issue

- Discussion