Funding for global health R&D in 2024

By Impact Global Health 5 February 2026

Key takeaways from the G-FINDER survey

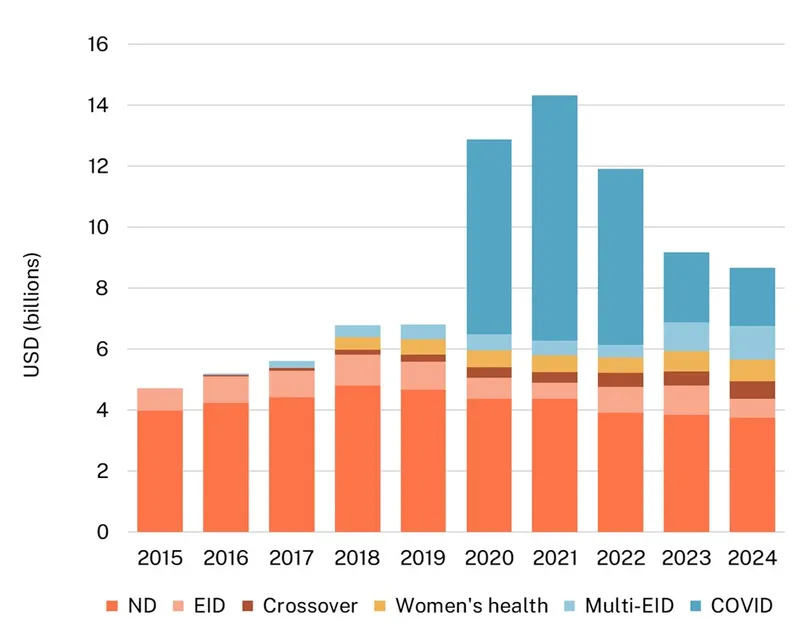

R&D funding by global health area, 2015-2024

Overall funding for global health R&D declined by a little under 6% in 2024, to $8.7bn, but three-quarters of the decline was due to reduced COVID funding

- Non-COVID R&D funding was down just 2% ($120m).

Funding specifically for neglected disease R&D fell slightly (by $98m, -3%) in 2024

- Funding for TB R&D continued to grow (up $41m, 5%), driven by Gates Foundation funding for M72 vaccine trials.

- Essentially all of the net drop in neglected disease funding was due to record-low HIV funding, which fell by a further $93m (-7%). HIV R&D funding has now fallen by nearly $500m over the past three years. Funding for malaria rose slightly, an increase of $25m (4%), taking it back to its 2021 level after a sudden drop in 2022.

Funding specifically for women’s health rose a little, by $29m (4%), thanks to rising spending on STIs, which more than offset falling HPV R&D

- There were substantial declines in funding for menopause (down $7.7m, -26%) and for multipurpose prevention technologies (down $13m, -45%); the latter is likely to continue into 2025 with the loss of funding from USAID.

Funding for non-COVID EIDs experienced a moderate decline in 2024 (of around $140m, or -7%) after growing by more than a third ($647m) in 2023

- There was a big shift away from multi-coronaviral R&D in favour of (much smaller) further increases in multi-EID funding. Non-COVID disease-specific EID funding fell by $83m (-15%), with further reductions for Ebola (down another $70m, or 42%) alongside more worrying cuts to Nipah (down $8.5m, -14%) and Marburg R&D ($19m, -25%).

The ongoing decline in COVID R&D slowed slightly, with spending falling by $383m (-17%) after dropping by nearly $6bn over the previous two years

- NIH COVID funding fell by a little over $200m (-29%) and is increasingly focused on basic research, which accounted for two-thirds of its COVID funding, up from less than 40% at the start of the pandemic.

'Crossover’ funding for more than one global health area rose by another $100m (22%)

- Multi-disease funding now accounts for almost 22% of global health R&D, more than any single disease.

Absolute (left axis) and percentage (right axis) change in funding by global health area

%20and%20percentage%20(right%20axis)%20change%20in%20funding%20by%20global%20health%20area-808x630.webp)

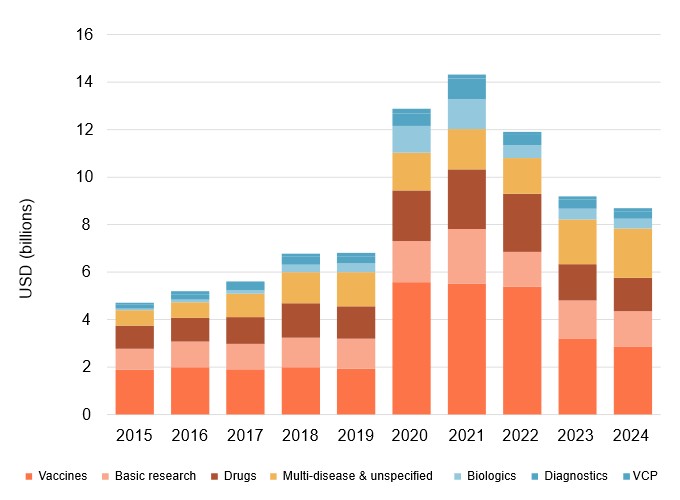

Product distribution of R&D funding, 2015-2024

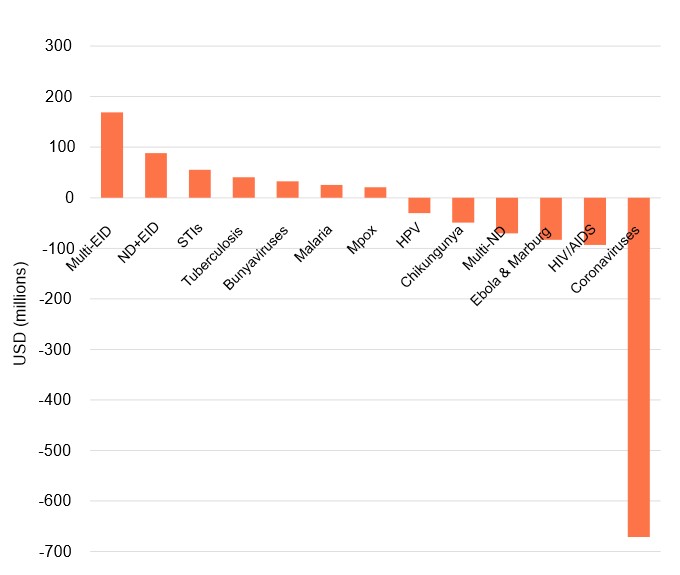

Areas with the largest absolute change in 2024

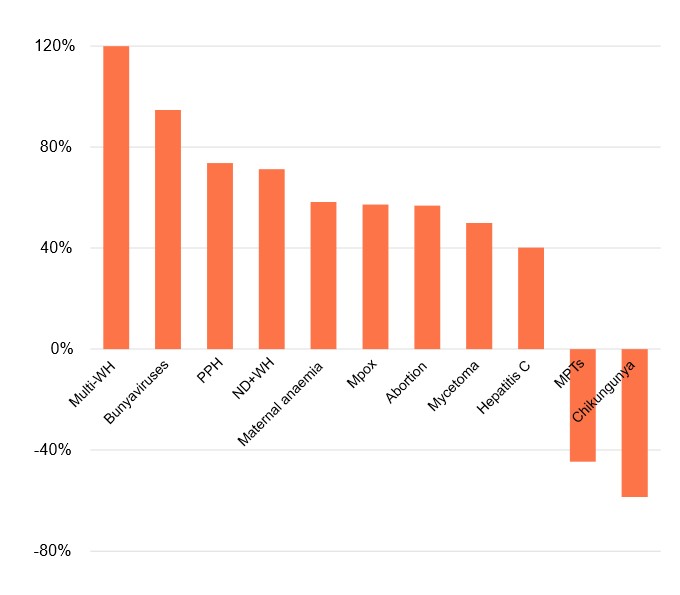

Areas with the largest proportional change in 2024

Analysis by global health area

Overall funding for global health R&D declined by 6% in 2024, but three-quarters of the fall was the result of reduced funding for COVID

- Non-COVID R&D was basically stable, falling by just under 2%, or around $120m.

- While overall global health R&D peaked in 2020/21, during the pandemic, non-COVID funding peaked in 2023, at $6.9bn, as spending on EIDs transitioned away from purely COVID-centric R&D to a range of multi-coronaviral and multi-EID projects.

Neglected diseases

Funding specifically for neglected disease R&D1 fell a little (down by just under $100m, or -3%) in 2024, following a similarly sized drop in 2023. This left funding at $3.75bn, more than a billion dollars below its 2018 peak.

HIV/AIDS

- A little over half this year’s fall was due to a slight reduction in funding from the US NIH (down by $54m, -3%), which has now fallen for five straight years. This, in turn, was due to another big reduction in the NIH’s HIV funding, which fell by a further $62m (-6%) and which is now nearly $300m below its peak in 2019.

- This reduction in NIH funding, along with a smaller drop from the Gates Foundation, saw overall funding for HIV fall sharply for a third consecutive year (down by $93m, or 7%, after falling by more than $150m in 2023). There were cuts to every product area, with the largest falling on HIV basic research (down $37m, -17%) and biologics (down $14m, -19%).

Tuberculosis

- Tuberculosis funding, on the other hand, repeated last year’s steady growth. TB R&D rose by a further $41m (5%) in 2024, thanks to another big increase in Gates Foundation funding for late-stage trials of the M72 vaccine candidate. TB vaccine funding rose by another third ($53m), taking it to $211m – nearly double its 2022 level. The Gates Foundation was responsible for three-quarters of this increase, with rising industry funding - largely for candidates other than M72 – accounting for most of the remainder.

- The Foundation’s TB R&D funding more than doubled from $137m in 2021 to $281m in 2024 – an increase of $145m, of which just over half has gone towards increased funding to the Gates Medical Research Institute (MRI) for late-stage trials of M72. Gates TB vaccine funding to the MRI reached a record $108m in 2024, up by more than $40m (67%) from 2023 – a fifth consecutive year of growth, with further increases expected in 2025.

- This pattern indicates a growing concentration of TB R&D around a single philanthropic funder and one late-stage vaccine asset, rather than broad-based increases across the wider TB pipeline. While this boosts the prospects for the successful introduction of a new vaccine – one intended for adult use – it also heightens portfolio risk, with opportunities to address the burden of TB increasingly reliant on the success of M72.

Malaria

- Malaria R&D funding experienced a small rise of $25m (4%), or around $38m after accounting for differences in survey participation. This second straight year of growth comes after four consecutive years of decline, which had led to a record low of just $668m in 2022. The 2024 increase was driven by rises in both drug and biologic R&D funding – with drugs up $32m (13%) and biologics more than doubling (up $26m, 107%) to a record $50m. The overall rise in malaria funding was largely driven by a $30m (31%) jump in industry drug R&D, alongside a smaller increase from the UK FCDO.

- While malaria funding grew only a little, an $85m grant from the Gates Foundation to the International Vector Control Consortium (IVCC), announced in 2024, had yet to begin disbursing funding in 2024, suggesting a likely future increase in chemical vector control for malaria and potentially offsetting the overall impact of 2025 reductions in US government malaria funding2.

- Taken together, our analysis suggests an early, still-fragile recovery from the 2022 trough. Most of the net gain is concentrated in a limited set of late-stage industry drug projects and a small number of biologic candidates. The expected ramp-up of the IVCC grant, therefore, suggests not only a further rise in overall malaria R&D over the medium term, but also a prospective rebalancing of the portfolio towards vector control after several years in which drugs have accounted for an increasing share of investment.

Other diseases

- Among the smaller neglected diseases, funding fell further for bacterial pneumonia & meningitis (down by $5.1m or -22%, continuing a longer-term decline), as did funding for rheumatic fever, cryptococcal meningitis and histoplasmosis. By contrast, hepatitis C funding rose by 40% ($8.5m), driven by a $5.1m (30%) increase in its NIH funding – which is now up by nearly $18m (400%) since 2020 – combined with the ramp up of a new 2023 funding stream from Open Philanthropy (now Coefficient Giving – up $2.4m to $2.8m). Diarrhoeal diseases R&D rebounded slightly, rising by $5.6m (4%), thanks to a rebound in industry funding from last year's record low and a big new stream of funding ($7.9) from Coefficient Giving, primarily focused on the development of a novel cholera vaccine. Despite this new investment, funding for cholera vaccines actually fell slightly, as Gates Foundation funding fell sharply following a two-year spike. Instead, the biggest beneficiaries of increased funding were Shigella vaccines (up $6.5m, 21%) and basic research (up $6.8m, 69%).

- These funding dynamics point to an increasingly bifurcated smaller-ND portfolio, with a narrow group of diseases (notably hepatitis C and some diarrhoeal pathogens) capturing most of the incremental funding while others remain on a sustained downward trajectory despite their ongoing burden.

Product development partnerships

- Funding to PDPs for neglected disease R&D finally rebounded slightly in 2024, growing by $12m (4%) from last year’s record low of $301m, returning it to roughly its 2022 level – still nearly $500m below its 2008 peak. A $23m (55%) rebound in PDP funding from the UK FCDO, an additional $6m from the Dutch DGIS and a (short-lived) $7m from USAID were enough to offset further steep cuts from the Gates Foundation (down around $33m, or 23%) and a smaller reduction from the NIH (down $4.4m, -21%) – which took both organisations' PDP funding to record lows. The largest beneficiaries of increased (ND-related) PDP funding were MMV and IVI, the latter seeing its funding more than double from last year’s record low.

- While ND-related PDP funding rebounded, substantial cuts to EID-related PDP funding (down $36m, -33%) meant overall funding to the sector declined by $21m (-5%).

- Even the modest rebound in ND-related PDP funding leaves them increasingly dependent on cyclical funding from a very small set of major funders, with the Gates Foundation continuing its long term shift away from grants to PDPs.

1 This excludes neglected disease-relevant ‘crossover’ funding applicable to more than one of our Global Health Areas, which we discuss separately below. That funding would normally be included in our headline G-FINDER neglected disease report totals. Including relevant multi-disease funding, overall ND funding was basically unchanged.

2 We have identified an annualised total of least $14m in NIH malaria grants terminated and not yet reinstated in 2025, excluding the impact of other policies.

Women's health

Funding specifically for women’s health3 rose slightly in 2024, increasing by $30m (4%) to a record $706m

Women’s health funding has now risen by $198m in two years, but around two-thirds of that growth resulted from the inclusion of seven new women’s health conditions in the survey. The scope-adjusted growth rate slowed a little in 2024, falling from 8% to 4%.

Sexually transmitted infections

- The net increase in women’s health funding is more than accounted for by the rise in funding for sexually transmitted infections (STIs), which has risen every year since the survey began, and which grew by a further $55m (25%) in 2024. Funding for chlamydia more than doubled (up $33m to $61m), accounting for most of the net growth in STI funding, but herpes simplex 2 continued to receive the largest share of STI funding, growing by $11m (13%) to $98m.

- Unlike other STIs, funding for human papilloma virus (HPV) and associated cervical cancer fell sharply, dropping by $30m (-24%) to a record low following big declines from the NIH (down 22%, $11m) and industry (down $16m, -37%).

Contraception and multipurpose prevention technologies (MPTs)

- Contraceptive R&D funding was essentially unchanged, with increases from industry and USAID enough to offset further cuts from both the Gates Foundation and the NIH.

- There was another steep reduction in R&D for multipurpose prevention technologies (MPTs), with substantial reductions from several major 2023 funders – headlined by a 37% ($6.1m) reduction from the NIH and a 92% ($1.8m) cut from the Gates Foundation. The headline estimate of a 45% ($13m) overall reduction is exaggerated by the lack of reporting from USAID – we were able to obtain their contraceptive funding data from recipients, but not data on MPTs – adjusting for their absence still suggests a $7.3m (31%) fall.

- Given the substantial role played by USAID for both contraception and MPTs in 2024, funding for both areas is likely to have declined further in 2025. We estimate that USAID was responsible for around 10% of global contraceptive funding in 2024, and potentially as much as 30% of overall MPT funding, little of which is believed to have survived its dissolution and the transfer of its remaining portfolio to the State Department.

Women’s and maternal health conditions

- Total funding for the women’s and maternal health conditions added to the survey last year was relatively unchanged, a 26% ($7.7m) fall in menopause funding offset by a $6.2m (17%) rise in preterm labour R&D and smaller increases in most other areas. While funding from the NIH – the main supporter of these areas – fell by $10m (-10%). This was more than offset by a $5.1m (900%) increase from the Gates Foundation and smaller increases from Coefficient Giving (formerly Open Philanthropy) and several other funders.

- Taken together, these shifts indicate that headline growth in women’s health R&D is being driven more by scope expansion and rapid increases in a small number of STI areas than by a widespread rising awareness of women’s health needs. The prospective loss of USAID as a major funder leaves the sector even more reliant on for-profit investment from industry, mostly focused on STIs, and early-stage funding from the NIH.

3 A category which now includes the gynaecological and maternal health conditions added to the survey in 2023.

Emerging infectious diseases

Overall non-COVID EID funding fell by 8% ($160m) in 2024, despite the further growth in multi-EID funding outlined below4

- Funding for individual (non-COVID) EIDs also fell substantially in 2024 – a drop of 17% ($95m) following a 20% fall in 2023.

- There were a number of changes in our survey’s scope this year, which influenced the headline total, including the removal of non-polio enteroviruses ($8.5m in 2023 funding) and SARS ($7.9m), more than offset by the addition of Hantaan virus ($7.8m in 2024) and avian influenza A (aka H1N1, $59m). Adjusting for these scope changes, disease-specific funding was down even further – by $145m, or 27%.

- These figures exclude $273m in funding provided by CEPI, which is not included here to avoid double counting the funding CEPI received. These disbursements from CEPI rebounded sharply from a low in 2023, rising by $68m (33%). CEPI’s COVID funding continued to decline, with its funding growth concentrated in Mpox and multi-EID grants, including vaccine platforms.

- Funding provided to CEPI rose by a further $55m (14%) to $457m and is now up by nearly $120m in the two years following the replenishment commitments it secured in 2022.

Ebola, Marburg and Mpox

- Much of the overall decline came via reductions in funding for Ebola (down by 42%, or $70m) and, more surprisingly, given its lack of approved products, Marburg (down by 25%, or $19m). Mpox funding rebounded by $21m (57%) but remained more than $20m below its peak in the immediate aftermath of the 2022 outbreak.

Crimean-Congo Haemorrhagic Fever, Rift Valley fever and Nipah

- Among the rarer diseases, there was an increase in R&D targeting the bunyaviruses Crimean-Congo Haemorrhagic Fever (up 73%, $9m) and Rift Valley fever (up 45%, $3.1m). At the same time, Nipah funding declined from last year’s peak, dropping by $8.4m, or 14%, following reduced disbursements from the DOD for biologics development.

H1N1 avian influenza and Hantaan virus

- The $61m in funding for the newly included H1N1 avian influenza came mostly from industry (53% of the total) and the NIH (32%) and focused heavily on vaccines (63% of funding) and basic research (31%). Hantaan virus funding came almost entirely from the NIH and was concentrated on biologics R&D.

Multi-EID funding

- Funding directed at more than one family of EIDs (‘multi-EID funding’) grew by nearly $700m between 2022 and 2024, and by $169m (18%) in 2024 alone

- Having reached well over $1bn in 2024, multi-EID R&D now accounts for almost two-thirds of (non-COVID) EID spending, up from just 5% in 2016.

- The shift of EID R&D towards multi-disease funding becomes even more pronounced once we include the rise in crossover funding for multiple global health areas – discussed below – and the share of funding focused on multiple diseases within a single viral family. This category of funding has grown nearly fourfold since the pandemic, increasing from $47 million in 2019 to $174 million in 2024. Partly, this growth reflects the sudden surge and subsequent decline in multi-coronaviral research that followed the initial wave of COVID-specific funding: multi-coronaviral R&D peaked at $345m in 2023 (up from just $4m pre-pandemic) before falling by four-fifths in 2024, in what is best seen as an extension of the wider decline in COVID funding discussed below. All other areas of viral family research gained ground in 2024, headlined by a 284% ($12m) increase in R&D for multiple arenaviruses – the family that includes Lassa fever.

- While the largest single share of the $169m 2024 increase in multi-EID funding came from the NIH, a substantial portion was the result of increased contributions from the US BARDA as part of its support for multi-disease vaccines under Project Next Gen, which was largely cancelled in 2025.

COVID

Funding for COVID R&D fell by another 17% (383m), leaving it at around a quarter of its 2021 peak

- Industry’s COVID funding fell by 41% ($417m), and funding from the NIH also continued to fall, by another $203m – following a much larger drop in 2023.

- Buffering these big declines was a somewhat surprising rebound in BARDA’s COVID funding, which rose by $408m (207%) as a result of the ramp-up of several large vaccine projects, which appear to have been subsequently cancelled in 2025 as part of the shift away from Project Next Gen.

- COVID drug and vaccine R&D each saw cuts of more than $100m in 2024, though this represented a much larger share of drug R&D, which fell by 55%. Diagnostic R&D also fell rapidly, dropping by 41% ($47m).

- The resulting shifts mean that the remaining interest in COVID R&D is increasingly split between vaccines, which received nearly two-thirds of 2024 funding, and basic research, which has seen its share rise from a low of 8% to 21% this year. Drugs, biologics and diagnostics each account for less than 6% of the total.

- Viewed as a whole, the 2024 data point to an EID portfolio in which most marginal growth is now flowing into multi-pathogen and platform-oriented work, at the expense of disease-specific programmes, especially those associated with past epidemics. The expansion of these multi-EID and cross-family investments is being driven largely by a small set of public funders, so both the overall level and configuration of future EID R&D will hinge on their budget and programme decisions, which we have already seen shift radically in 2025. For COVID, the shift in the funding mix towards vaccines and basic research, with only limited residual support for other product types, indicates that ongoing effort now closely resembles R&D for an endemic disease, rather than the variety of approaches that characterised the initial R&D response to the pandemic.

4 These figures do not include dengue, which we now treat as both an EID and a neglected disease. To avoid double counting, dengue funding is captured exclusively under neglected disease R&D

Funding applicable to more than one global health area

‘Crossover’ funding for more than one global health area (GHA) rose by another $100m (22%) to 566m

- This funding has grown more than tenfold since we began tracking it in 2016. It now accounts for almost 7% of global health R&D, only slightly below the 8% devoted specifically to women’s health.

- Alongside the growth in multi-GHA funding have been ongoing increases in funding targeting more than one disease within a single global health area – much of which is intended to combat multiple EIDs. This kind of multi-disease funding grew by $100m (10%) in 2024 alone, and by more than $1bn since 2015. This means that overall multi-disease funding accounted for over a fifth of 2024 funding: broadly in line with the 22% devoted to COVID, and substantially more than the 14% devoted to HIV.

- Multi-disease funding within a single global health area is even more skewed towards EIDs, which account for more than 80% of this funding, with multi-neglected disease funding accounting for almost all the remainder, and funding targeting more than one SRH area receiving less than 3% of the total.

- Recent growth in multi-disease approaches to R&D – both within and across global health areas – is largely a result of increased spending from the US government, particularly the DOD. It more than doubled its multi-disease (mostly platform) funding in 2023 and increased it by a further $59m (12%) in 2024, making it the largest single funder in both years. Multi-disease funding from the NIH also continued to grow, rising by another $55m (22%) to exceed $300m – more than four times its pre-COVID total.

- Overall, the rapid expansion of crossover and multi-disease funding shows that an increasing share of global health R&D is now channelled through platform and multi-pathogen mechanisms, with a growing proportion of this support provided by a small number of US government agencies, particularly the DOD and NIH. These will ultimately need late-stage funding to adapt them to specific pathogens, potentially including as-yet-unknown EIDs.