The diagnostics deficit: Funding, access, and preparedness gaps in African health systems

By Impact Global Health and PATH 16 July 2026

Key messages

- Diagnostics are foundational to Africa’s epidemic preparedness, surveillance, and primary health care systems, enabling timely treatment, outbreak detection, and outbreak containment. However, they remain underprioritized in health security planning and investment relative to their importance, with only 19% of patients having access to appropriate diagnostics at the primary care level.

- For the six Africa CDC priority diseases analyzed, diagnostic research and development (R&D) funding targeting mpox, dengue, cholera, meningitis, malaria, and Ebola has declined by nearly US$4 million, or around 7%, annually since 2015 (data current to 2024).

- The challenge is no longer only product development. Across these six diseases, 577 diagnostic products are already approved, and 59 remain in active development, but the landscape is heavily concentrated in dengue and mpox. The priority now is to ensure that available diagnostics are affordable, accessible, and deployable in the settings where they are needed most.

- Approval does not guarantee frontline access. Around half of approved diagnostics require clinical laboratory infrastructure, limiting their use in primary health care settings where many patients first seek care.

- Africa needs a clearer, fit-for-purpose diagnostic product roadmap, aligning R&D, supporting World Health Organization (WHO) target product profiles that account for LMIC end use, regulatory pathways, and deployment priorities with continental disease burden and health security needs. The African Medicines Agency (AMA) represents the most significant structural opportunity to deliver this.

- Africa’s diagnostic manufacturing base exists, with installed capacity to produce more than 500 million diagnostic units annually. However, regulatory fragmentation, weak demand signals, and capital barriers continue to limit its viability and scale. The constraint is not infrastructure alone, but the ecosystem support needed to translate capacity into sustainable production.

Introduction

As heads of state convene an AU Extraordinary Health Summit in Accra to commit to ending AIDS by 2030 and tackling preventable maternal deaths and outbreak-prone diseases, this report asks a foundational question: Does Africa have the diagnostic systems needed to deliver on those commitments? The evidence suggests not yet—but the gap is closeable.

Specifically, this report examines whether Africa’s diagnostic development, regulatory systems, and manufacturing capacities are aligned with the continent’s health security agenda. It does not attempt to map the entire diagnostics landscape. Instead, it places a deliberate spotlight on specific system readiness challenges, exploring where political commitments on diagnostics have been made, whether current systems are positioned to deliver on those commitments, and what needs to change.

The report is structured around six interconnected issues, each representing a current failure or underexplored gap: diagnostic R&D investment; pipeline alignment with Africa’s priority diseases; the access-not-just-innovation gap; the regulatory environment; manufacturing feasibility; and the linkages between diagnostics, surveillance, and primary health care. Taken together, they point toward a continent that has political commitments in place but has not yet built the systems to honor them.

Strategic context: Why diagnostics matter now

Diagnostics as foundational health infrastructure

Without diagnostics, health systems are forced to act in the dark. Although a surveillance system may first detect early signs of an outbreak through syndromic or event-based reporting, diagnostics are still essential before laboratory confirmation is available. They are often needed before a patient can reliably receive the right treatment, before a suspected case can be confirmed, and before the early warning signal can be accurately classified and acted on. When that test is absent, inaccurate, or inaccessible, the consequences cascade across the health system. The May 2026 Bundibugyo ebolavirus outbreak illustrates this gap starkly. Ten days were lost in the response because initial samples tested negative with assays designed to detect the Zaire ebolavirus, while the outbreak was caused by the Bundibugyo ebolavirus. Pan-ebolavirus tests that can detect Bundibugyo exist in principle, but very few Bundibugyo-specific diagnostics are available, and the right tools were not available at the point of need. These diagnostic readiness gaps are particularly concerning in Africa, which carries a disproportionate share of the world’s infectious disease burden, including most global malaria deaths and recurrent outbreaks of Ebola and mpox.1 At the same time, the continent remains structurally dependent on diagnostic tools that are often developed, manufactured, validated, or approved primarily outside Africa, even though country-level validation and regulatory approval are still required for use on the continent. The HIV response offers an instructive parallel: the deployment of point-of-care diagnostics and decentralization of testing across sub-Saharan Africa, which is home to over two-thirds of all people living with HIV, demonstrates what coordinated investment in diagnostic infrastructure and supply chain decentralization can achieve for infectious disease prevention and control at scale. Yet, even within the HIV diagnostic landscape, access to rapid testing remains unequal across the region.

For many priority diseases, especially emerging and outbreak-prone infections, access to diagnostics remains constrained by affordability, regulatory fragmentation, limited local validation, and dependence on external supply chains. Africa carries a dual burden of persistent endemic diseases and recurring epidemic threats while still lacking reliable access to the full range of diagnostics needed to detect and respond effectively to both.

This challenge is becoming increasingly urgent because of several converging forces. Climate-sensitive diseases such as dengue and chikungunya are becoming increasingly important as insect vectors expand their geographic range, bringing clinically similar infections into populations with limited prior exposure and weak diagnostic infrastructure to differentiate them. At the same time, many countries continue to rely on empirical treatment for common infections, which can contribute to inappropriate antibiotic use and increasing resistance among pathogens.

Africa CDC’s prioritization of diseases for diagnostic development and deployment reflects a clear recognition that diagnostic access is central to the continent’s health security agenda. The list helps identify where improved diagnostic availability, performance, deployment, and manufacturing readiness are most urgently needed. Against this backdrop, this brief assesses whether current diagnostic R&D, regulatory systems, and manufacturing capacities are aligned with Africa’s risk profile and diagnostic priorities. It identifies critical gaps across the diagnostic ecosystem while highlighting opportunities to strengthen detection, improve access, and build more resilient health systems across the continent.

1 HIV is not among the six priority diseases analyzed in this brief, but it illustrates the same point: roughly two-thirds of all people living with HIV reside in sub-Saharan Africa. Source: UNAIDS.

Diagnostic R&D investment: Structurally low and declining

Diagnostic R&D for Africa CDC’s priority list of diseases

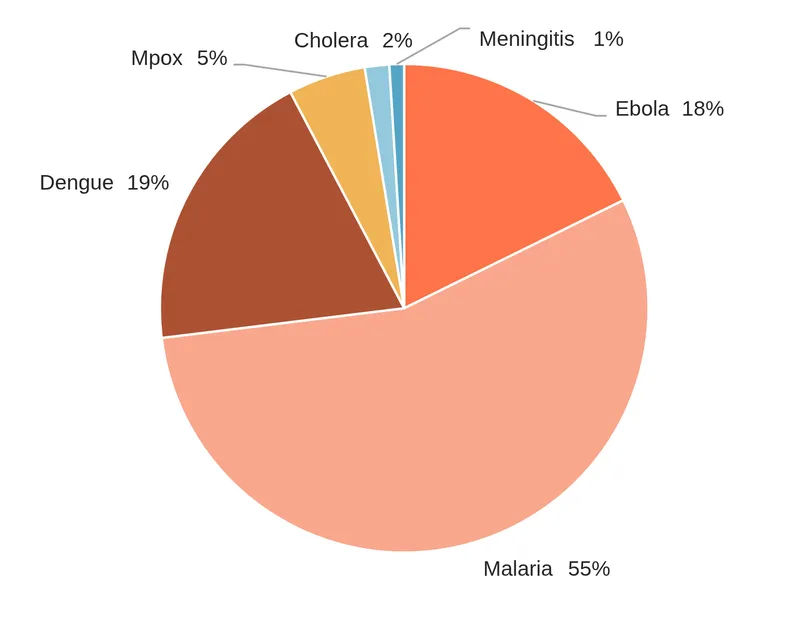

This analysis focuses on Africa CDC’s priority diseases for which G-FINDER data are available—mpox, dengue, bacterial meningitis, and cholera2—along with malaria and Ebola, the two pathogens with the largest non-COVID investments in diagnostic R&D captured by G-FINDER over the past 10 years. G-FINDER data capture annual global health R&D investment reported by public, philanthropic, not-for-profit, and industry funders. However, industry coverage can often be incomplete and depends on companies’ participation in the survey. As a result, the figures presented here should be interpreted as reported global health R&D investment captured by G-FINDER rather than a complete estimate of all diagnostic R&D activity. This limitation is particularly relevant for diseases such as dengue, where a sizable commercial diagnostics market exists, and company-funded product development may not be fully reflected in the data. Looking at these six priority diseases, most reported funding has gone to malaria diagnostics, with much of the remainder split between dengue and Ebola. Smaller shares have been reported for mpox, cholera, and bacterial meningitis diagnostics (Figure 1).

Figure 1: Funding for diagnostic R&D, Africa CDC priorities plus Ebola and malaria, 2020–2024.

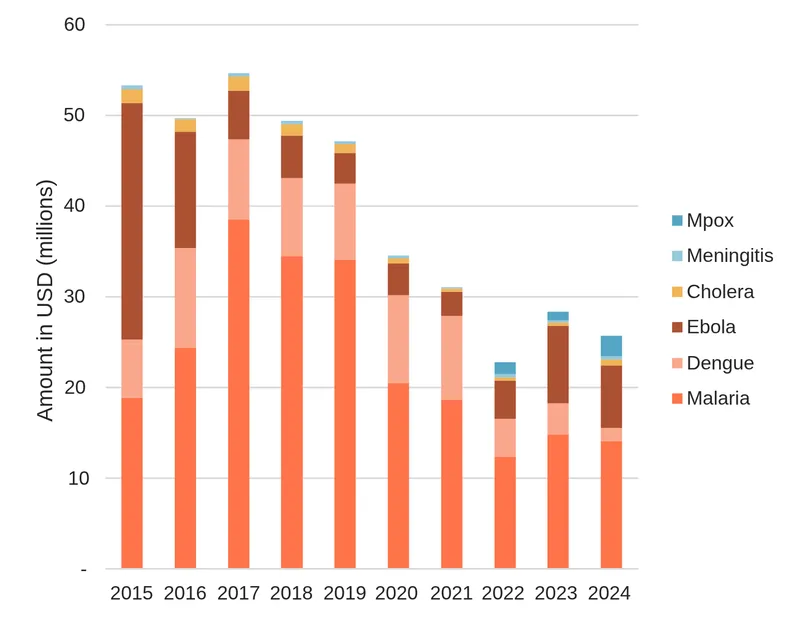

When assessed over time, the pattern is different. Overall funding across this group of diseases has trended down by nearly US$4 million a year, from a high of nearly US$55 million to just under US$26 million in 2024, despite the 2022 addition of mpox to the list of diseases covered (Figure 2).

Figure 2: Funding for diagnostic R&D by year, 2015–2024.

Diagnostic R&D has trended down across all diseases, except post-outbreak mpox and meningitis, which account for a trivial share of overall funding. The steepest proportional falls have been for Ebola—down from a peak of US$26 million in 2015 to less than US$7 million—and cholera, which had fallen from around US$1.5 million a year a decade ago to US$360,000 in 2023 before rebounding slightly in 2024.

The fall in Ebola diagnostic R&D funding likely reflects the passing of the 2014–2016 West African epidemic and the 2019 Democratic Republic of the Congo (DRC) outbreak, as well as the successful registration of diagnostics following these events. However, the 2026 Bundibugyo outbreak underscores the risks of an outbreak-driven funding model, where investment declines between crises despite the need to maintain readiness, adapt tools to emerging strains, and ensure rapid deployability in affected settings. Falls for the other diseases, particularly cholera, are more concerning and may suggest waning interest in sustained investment in diagnosis and access.

How disease trends should inform diagnostic priorities

Disease burden and incidence are important contexts for diagnostic R&D, procurement, and deployment decisions, but they do not, on their own, determine R&D need. Rising incidence should help guide which diagnostic tools countries make available, procure, and prioritize, and where they are deployed to support more efficient use across primary health care, surveillance, and outbreak response systems. Prioritization must, however, account for outbreak potential alongside incidence trends. A pathogen with infrequent historical occurrence may still warrant significant diagnostic investment if its epidemiological characteristics or transmission dynamics point to disproportionate risk should an outbreak occur. The ongoing Bundibugyo ebolavirus in some African countries is a clear example: its low historical incidence would not have signaled urgent need, yet its close relationship to Zaire ebolavirus makes diagnostic unpreparedness a risk that far exceeds what the historical record implies. Thus, readiness, in this sense, is not a function of how often a pathogen has caused outbreaks, but of what it could do if it did.

Where effective, affordable, and deployable diagnostics already exist, the priority may be to expand access, strengthen procurement, assure quality, and integrate testing into routine care. Where existing tools are absent, poorly adapted, too costly, insufficiently accurate, or vulnerable to changes in pathogen biology, targeted R&D may still be needed.

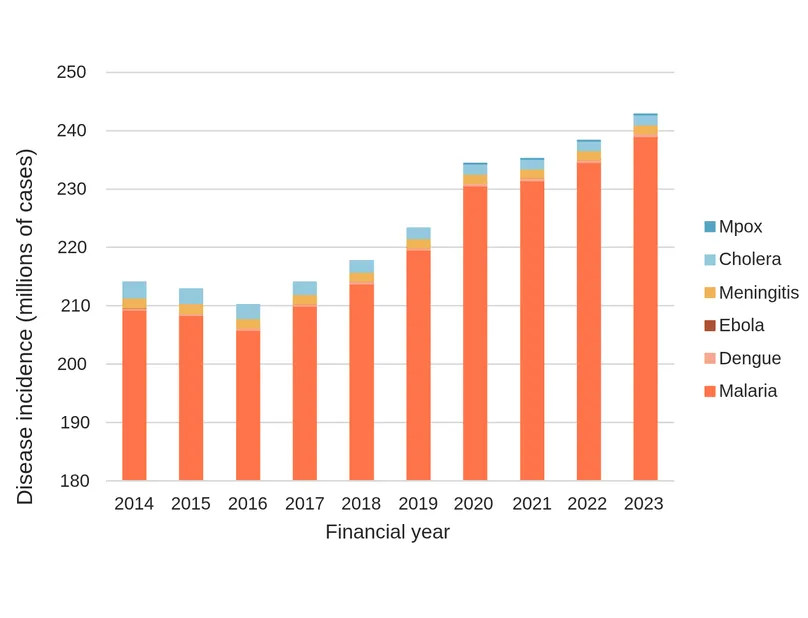

Across the diseases considered in this report, epidemiological trends indicate ongoing and, in some cases, renewed pressure on diagnostic systems. While Ebola cases had fallen sharply following the end of the major DRC epidemic in 2025, the 2026 Bundibugyo virus outbreak in DRC and Uganda, barely six months later, underscores the continuing risk of sudden resurgence, cross-border spread, and uncertainty in the early stages of outbreak detection. At the same time, reported cases of dengue, malaria, and mpox in Africa have trended upward over the past decade (Figure 3). These trends do not imply that diagnostic R&D should automatically increase in line with incidence. Rather, they highlight the need to assess whether the right diagnostic tools are available, validated, procured, prioritized, and rapidly deployable in the settings where they are needed most, including during outbreaks where the true scale may not yet be known.

Figure 3: Priority disease incidence, 2014–2023.

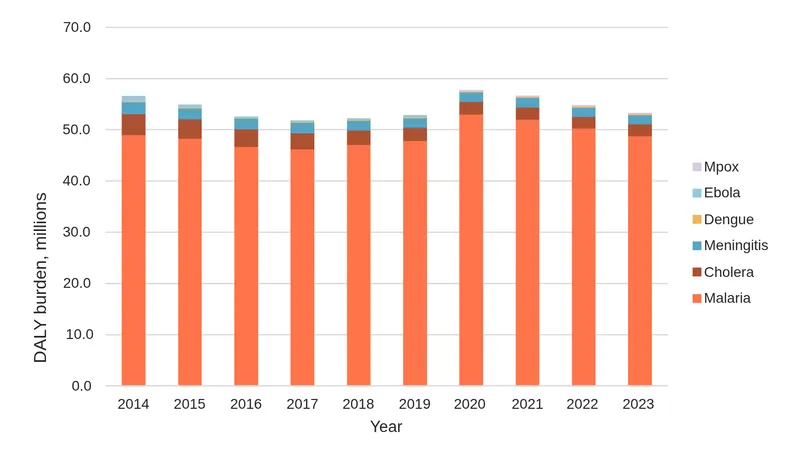

Despite the rising number of reported cases for some diseases, Africa’s disability-adjusted life-year (DALY) burden from this group of diseases has remained relatively stable over the same period, as shown below (Figure 4).

Figure 4: Disability adjusted life-year (DALY) burden of priority diseases in Africa, 2014–2023.

DALY trends reflect a combination of factors, including changes in case fatality, treatment access, disease management, prevention efforts, reporting practices, and the relative contribution of different diseases to the overall burden. For malaria, for example, declining case fatality has helped offset rising case numbers, while case fatality rates have also fallen for dengue and bacterial meningitis.

This pattern suggests that some gains have been made in preventing illness from progressing to severe disease or death. However, those gains are uneven across diseases and settings, and they do not eliminate persistent gaps in diagnostic availability, quality, affordability, and access.

Sustaining gains in survival and reducing DALY burden will require continued access to rapid diagnostics, effective treatment, and primary health care. At the same time, rising incidence signals the need to strengthen upstream prevention measures, including vector control, vaccination where available, and outbreak control, while ensuring that diagnostic tools are deployed in the right places, for the right diseases, and at the right level of the health system.

2 The Africa CDC list also includes measles; a pathogen not covered by Impact Global Health’s funding or pipeline data and so is omitted here.

The diagnostic R&D pipeline: Innovation is not translating evenly into access

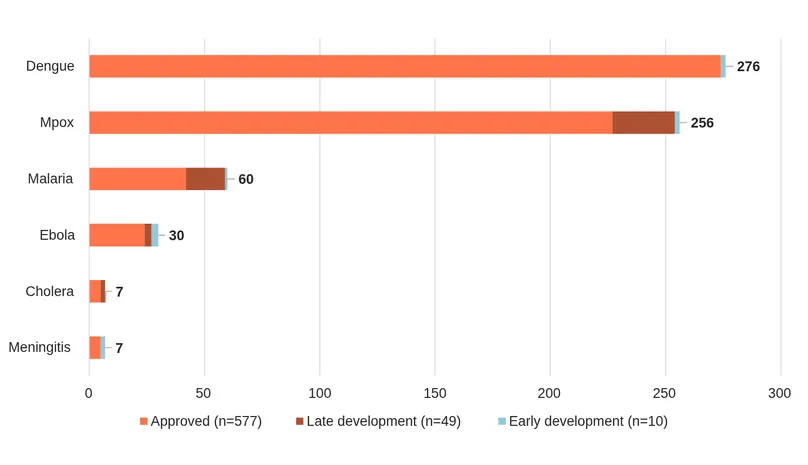

The assumption that Africa’s priority diseases lack robust diagnostic pipelines is only partially true, and the nuance matters. Across the six diseases considered in this report, Impact Global Health’s Product Pipeline Portal shows 577 products already approved and 59 candidates in active development. The diagnostic challenge is therefore not primarily whether products exist. For several diseases, the more pressing question is whether approved tools are affordable, quality-assured, operationally feasible, and accessible where patients seek care and where outbreaks need to be detected.

Figure 5: Active diagnostic pipeline by disease and development stage, 2025.

An approved but unevenly distributed landscape

The approved3 product landscape is markedly uneven. Dengue and mpox dominate the portfolio, together accounting for 532 products and candidates, or 84% of the total across the six diseases, while the remaining four diseases collectively account for 104 products and candidates. Cholera and bacterial meningitis, both highlighted in Africa CDC’s priority list and relevant to antimicrobial resistance (AMR) and outbreak preparedness, have only seven products and candidates each.

Across all six diseases, the proportion of products already approved ranges from 70% for malaria to 99% for dengue. Taken together, the pattern points to a landscape in which scientific innovation has, in many respects, already delivered a substantial base of tools, particularly for better-resourced or higher-profile disease areas. Yet this progress is unevenly distributed and does not automatically translate into access or impact.

This is where the innovation and access gap becomes clearest. A diagnostic product can be approved and still fail to meet public health needs if it is too expensive, too dependent on central laboratory infrastructure, unavailable through procurement systems, poorly aligned with frontline use, or not adapted to local epidemiological and health system contexts. In other words, approval is an important milestone, but it is not equivalent to access, usability, or public health impact.

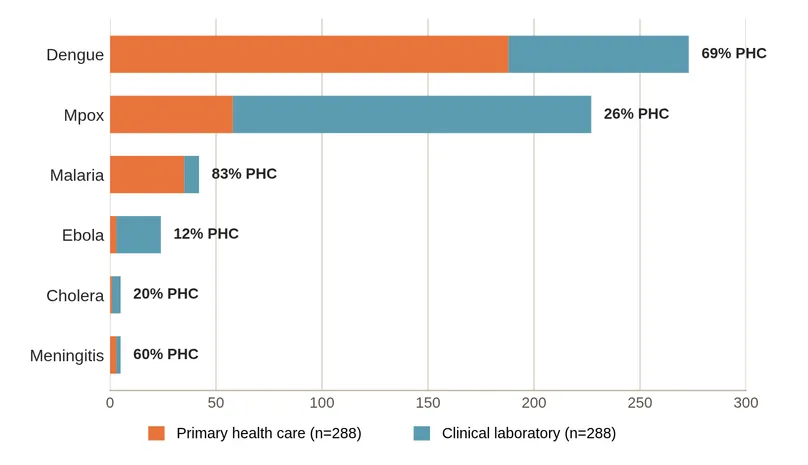

Half of the approved diagnostics remain lab-bound

Of the 577 approved diagnostics across the six diseases, 288 require clinical laboratory infrastructure, meaning that around half of the approved diagnostic toolkit cannot easily reach the primary health care level, where many patients first present.

The extent of this constraint varies considerably by disease. Approved mpox and Ebola diagnostics are overwhelmingly lab-dependent, with 74% and 88%, respectively, requiring laboratory infrastructure. This limits their reach in frontline settings and can slow detection and response when samples need to be transported to central facilities. In contrast, malaria diagnostics are far more decentralized, with 83% suitable for primary health care settings, reflecting sustained investment in rapid diagnostic technologies and deployment strategies. Dengue sits between these examples, with 69% of approved diagnostics suitable for primary health care use (Figure 6). Not every diagnostic needs to sit at the point of care: centralised laboratory testing can offer advantages for quality assurance, data reporting and cost-effective surveillance. The concern is rather the absence of decentralised options for the diseases and settings where rapid frontline detection is time critical.

These differences show that Africa’s capacity for early detection and response varies significantly by disease.

Figure 6: Approved diagnostics by deployment setting, 2025.

An outbreak-shaped, not continuously strengthened, pipeline

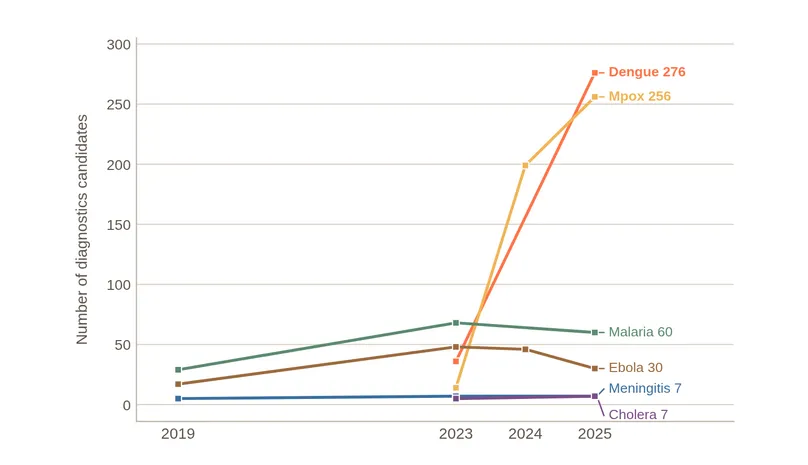

The overall figure of 636 products and candidates should also be interpreted carefully. It reflects recent and episodic expansion in some disease areas rather than steady, cumulative growth across all priority diseases. The clearest example is mpox. Following the 2022 outbreak, the mpox diagnostic landscape expanded rapidly, with 177 approved mpox diagnostics now captured in the database. This surge reflects how quickly diagnostic development can respond when global attention, demand, and investment increase.

Outside of mpox, the picture is closer to a plateau than progress. For example, the Ebola diagnostic pipeline has remained largely unchanged, with 17 late-stage and 10 early-stage candidates reported consistently across 2023 and 2024, suggesting limited progress through the development stages. More broadly, the pattern suggests a system characterized less by continuous pipeline strengthening and more by bursts of activity linked to outbreaks.

This matters for Africa because endemic and recurrent epidemic threats require sustained diagnostic readiness, not only emergency-driven innovation. Epidemic-prone diseases may attract attention during crises, but maintaining diagnostic capacity between outbreaks is essential for preparedness.

Figure 7: Active diagnostic candidates per disease, 2019–2025.

Limited strategic guidance for half the pipeline

World Health Organization (WHO) target product profiles (TPPs) define the desired characteristics of diagnostics for specific diseases and use cases, providing reference points for product developers, funders, and procurers by clarifying the type of diagnostic needed, where it should be used, and what performance standards it should meet. Among the six priority diseases, only three have relevant WHO TPPs: bacterial meningitis surveillance (April 2024), two mpox profiles for laboratory and decentralised use (July 2023), and a malaria G6PD screening profile (November 2022). Cholera, dengue and Ebola currently lack corresponding TPPs. As a result, 49% of the active pipeline operates without a clearly defined product specification framework.

Even where TPPs exist, alignment is not guaranteed. Within the mpox laboratory-use profile, only a small number of candidates fully meet the preferred criteria, including more demanding specifications such as integrated systems capable of differentiating clades I and II. A large pipeline does not necessarily mean that development activity is converging around the most valuable public health use cases.

The pipeline data challenge a simple scarcity narrative. For five of the six diseases discussed, approved products account for more than 70% of the total pipeline. The problem is therefore not primarily a lack of approved diagnostics. The more pressing issues are whether approved tests can reach the settings where patients present, whether active development continues between outbreaks, and whether innovation is guided by clear public health use cases aligned to African needs. The next phase of diagnostic policy cannot focus solely on discovery; it must also address deployment, affordability, regulatory alignment, quality assurance, procurement, manufacturing readiness, and integration into primary health care and surveillance systems.

3 In this brief, 'approved' refers to regulatory authorization captured in the Impact Global Health database – for example, authorization by a recognized stringent regulatory authority, WHO Prequalification (PQ) or WHO Emergency Use Listing (EUL).

The regulatory environment: Fragmented, misaligned, and under-resourced

Diagnostics are the entry point to care and directly shape treatment decisions, disease control, and surveillance outcomes. Yet from a regulatory standpoint, they occupy a persistently underrecognized position. Historically, regulatory pathways bundled diagnostics with pharmaceuticals or, more recently, with medical devices despite diagnostics having distinct regulatory requirements, market dynamics, and evaluation frameworks. This has limited their development, delayed approval, and constrained integration into care pathways.

The legislative and policy frameworks for diagnostics in Africa are fragmented and multilayered, operating simultaneously at continental, regional, and national levels, with significant inconsistency across all three. Although diagnostics and medical devices share some regulatory overlaps, they are not equivalent. Diagnostics are defined by their intended function (detecting, measuring, or monitoring a biological state), while medical devices encompass a broader legal category that includes nondiagnostic equipment for treatment, prevention, and monitoring. Bundling diagnostics into medical device frameworks can obscure the specialist expertise required to evaluate diagnostics and has contributed to inconsistent, unpredictable regulatory treatment.

National regulatory authorities (NRAs) across Africa also lack the technical capacity and regulatory expertise needed to evaluate diagnostics effectively. Premarket assessment of diagnostics remains limited, with the main constraints cited as insufficient technical and scientific expertise within NRAs, the high cost of evaluations, and difficulty obtaining licenses to apply international standards. With limited specialization and continued regulatory fragmentation, consistent and timely access to diagnostics across the continent will remain constrained.

Diagnostics used in disease-specific programs such as malaria and HIV have well-developed regulatory processes, largely because international organizations provide both the tools and the regulatory support as part of their programs. This model has produced islands of regulatory maturity surrounded by weaker, less predictable pathways for products outside of donor-prioritized disease areas. It demonstrates the limitations of vertically driven donor support and points to the need for broader systemwide investment by African governments and institutions in diagnostic regulatory systems that are cross-cutting and equitable across diseases.

For locally manufactured diagnostics, regulatory fragmentation is a key constraint. Manufacturers must comply with multiple national regulatory systems, resulting in duplicated reviews, higher costs, and delayed market entry. This disadvantage falls disproportionately on local manufacturers, who lack the global registration teams and resources that large multinationals deploy as a matter of course. The asymmetry is further reinforced by limited access to clinical data, reliance on imported inputs, and procurement practices that undervalue quality-assured local products.

African Medicines Agency as a structural opportunity

Regulatory harmonization represents the clearest systemic opportunity to address these constraints. Through the African Medicines Agency (AMA), coordinated and accelerated approval pathways can reduce duplication, shorten time-to-market, lower costs, and improve regulatory confidence across the continent. However, for diagnostics specifically, AMA must go beyond general harmonization. It has a unique opportunity to establish diagnostics as a distinct regulatory category with dedicated evaluation pathways that are not subsumed under medical devices, and to develop continent-wide standards that cut across diseases rather than reproducing the vertical program model. A streamlined regulatory environment is essential for enabling local innovation, strengthening market access, and expanding the availability of quality-assured diagnostics across Africa. Evidence generated throughout this report may inform potential recommendations by national/regional public health authorities (e.g., Africa CDC) or support submissions for regulatory authorization (e.g., WHO emergency use listing, African Medicines Agency Continental listing procedure).

Manufacturing feasibility: Capacity exists, but the ecosystem does not

Africa’s diagnostics ecosystem remains highly dependent on imports, exporting only US$1 in diagnostics for every US$93 imported (PATH MADE Analysis)4. Locally developed products rarely progress from early-stage research to commercialization scale. This weak pipeline limits the availability of diagnostics tailored to African contexts and hinders the development of a sustainable manufacturing base needed for equitable access and pandemic preparedness.

Current manufacturing capacity

Diagnostics manufacturing capacity across the continent is still nascent. However, local entrepreneurs and technology transfer partners have been making the investments needed to compete in continental and global markets. Codix in Nigeria has partnered with SD Biosensor to build a large manufacturing facility outside Lagos, while Microhaem in Uganda and Revital in Kenya have invested heavily in production facilities that could, in the coming years, supply hundreds of millions of diagnostics to global markets. Installed capacity across the continent is sufficient to produce more than 500 million diagnostic units per year. However, without technical support, demand, and financing, these factories may not become commercially viable.

Technical barriers

No large diagnostic factory in Africa is yet operating at scale, as many products lack the regulatory approvals needed to compete in major global markets. The limited availability of locally generated clinical and performance data further complicates regulatory review and slows product approval. Many manufacturers also lack experienced clinical affairs teams to coordinate studies and generate evidence, as well as regulatory affairs teams to prepare strong dossiers and respond to regulators’ queries. In addition, quality management systems often need strengthening to meet site inspection requirements consistent with regulatory requirements such as WHO Prequalification, which is essential for access to major donor procurement markets.

Demand barriers

Demand signals from global health institutions for African-made diagnostics remain weak, leaving manufacturers with too little certainty to justify long-term investments that may take years to yield returns. The US President’s Emergency Plan for AIDS Relief (PEPFAR) had previously signaled its intention to procure African-made HIV rapid diagnostic tests, prompting manufacturers to invest millions of dollars in new facilities and products. Subsequent changes in funding priorities have made that demand less certain. African diagnostic manufacturers need firm demand commitments, not vague signals, from institutions such as the Global Fund and, in the future, the Africa Pooled Procurement Mechanism so they can invest without risking financial collapse.

Financing barriers

Diagnostic manufacturers in Africa particularly face acute capital constraints that make it difficult for them to compete with large multinational companies. First, developing and commercializing a diagnostic typically takes more than three years before entering the market; in the meantime, manufacturers need sufficient cash to cover development, evidence generation, regulatory fees, and other fixed costs. These challenges are particularly acute for African manufacturers, many of which have limited access to affordable capital, because investment risks in Africa are often perceived as unfairly high, making it harder to qualify for commercial financing or resulting in very high interest rates. Lastly, payments from customers, especially governments, can be significantly delayed, and many manufacturers cannot afford to tie up large amounts of working capital while awaiting payment.

Unitaid has funded the PATH-led Manufacturing to Accelerate Diagnostic Excellence (MADE) project (2025–2029) to provide direct technical and financial support to five African manufacturers while strengthening the R&D and regulatory ecosystem and generating demand for African-made diagnostics. MADE addresses the technical, demand, and financial barriers outlined above through a catalytic investment model designed to de-risk manufacturers and attract investment from private investors and development finance institutions. However, sustained support from AU institutions, African governments, and global health organizations will be essential to scale impact beyond the five-company portfolio.

4 Source: PATH, Manufacturing to Accelerate Diagnostic Excellence (MADE) analysis (forthcoming). These figures are drawn from a PATH analysis that is not yet publicly released; the methodology and permission to cite should be confirmed before publication.

Surveillance, preparedness, and primary health care linkages

Diagnostics are foundational to effective surveillance and preparedness systems, enabling early case detection, data generation, and timely public health response. Africa CDC and member state institutions have emphasized the need to integrate diagnostics into national and regional surveillance frameworks. In practice, however, significant gaps remain at both surveillance and primary care levels.

Surveillance and preparedness gaps

Across many African countries, outbreaks are often detected late due to both limited availability of appropriate diagnostics and limited access to rapid diagnostics, driven by weak surveillance systems. For example, during early Ebola virus disease outbreaks, initial cases were sometimes misdiagnosed as malaria or typhoid, which delayed response and containment. In rural areas of countries such as the Democratic Republic of the Congo, patient samples often need to be transported long distances to central laboratories, which can delay confirmation of diseases such as cholera or mpox for several days. During the COVID-19 pandemic, limited genomic sequencing capacity across the continent meant that only a few countries, such as South Africa, could rapidly identify variants like Beta, while many others relied on external laboratories for analysis. The May 2026 Bundibugyo Ebola outbreak has also highlighted how diagnostic readiness gaps can undermine outbreak response, even where surveillance systems are more alert to unusual disease events because of past outbreaks. Reports suggest that delays in laboratory confirmation, including challenges linked to strain-specific diagnostic testing capacity, may have slowed early containment efforts. These challenges, compounded by insecurity, population movement, and weak health infrastructure, illustrate that preparedness depends not only on detecting outbreaks but also on having accessible, adaptable, and rapidly deployable diagnostic systems in place.

This is particularly important in the context of the 7-1-7 target for outbreak preparedness, which calls for detecting an outbreak within seven days, notifying it within one day, and responding within seven days. Without timely and reliable diagnostics, countries can face delays in detection and case confirmation, undermining rapid response efforts. In addition, weak and often paper-based data systems in some settings delay the aggregation and sharing of surveillance information, reducing the ability of health authorities to respond in real time.

Primary health care linkages

At the frontline of care, diagnostics are often not fully integrated into routine primary health care services, particularly in rural and underserved areas. For instance, in parts of Kenya and Uganda, patients presenting with fever are frequently treated presumptively for malaria because rapid diagnostic tests are unavailable or out of stock, increasing the risk of misdiagnosis. In many primary health facilities, unreliable electricity and limited infrastructure restrict the use of basic laboratory equipment, affecting the diagnosis of diseases such as tuberculosis. Workforce constraints also play a role, as community health workers may lack training in the use or interpretation of newer diagnostic tools. In addition, weak referral systems can delay confirmation of conditions such as cervical cancer, where patients must be referred to higher-level facilities for testing, and results are often slow to return.

System-level implications

These weaknesses reinforce broader R&D and access gaps by limiting the generation of real-world diagnostic data, reducing demand visibility, and weakening feedback loops between innovation, regulation, and health system needs. A diagnostic tool’s public health value depends not only on its technical performance but also on whether it is integrated into care pathways and surveillance systems in ways that enable its efficient and equitable use. Strengthening diagnostic integration across surveillance and primary care is therefore critical to improving preparedness, reducing systemic risk, and enabling more responsive and resilient health systems.

Malaria rapid diagnostic tests (RDTs) illustrate what is possible when diagnostics are developed, procured, and deployed at scale. A 2024 JAMA study across 35 sub-Saharan African countries found that wider distribution of malaria RDTs was associated with increased blood testing, increased use of antimalarial treatment, and modest improvements in child survival. At a weighted average price of around US$0.36 per test (UNICEF), malaria RDTs demonstrate how affordable diagnostics can support large-scale primary health care delivery when procurement, supply, and integration systems function effectively. The challenge for Africa’s broader diagnostic agenda is to replicate the conditions that made this possible across more diseases, at more levels of the health system, and with stronger feedback between field deployment and R&D priorities.

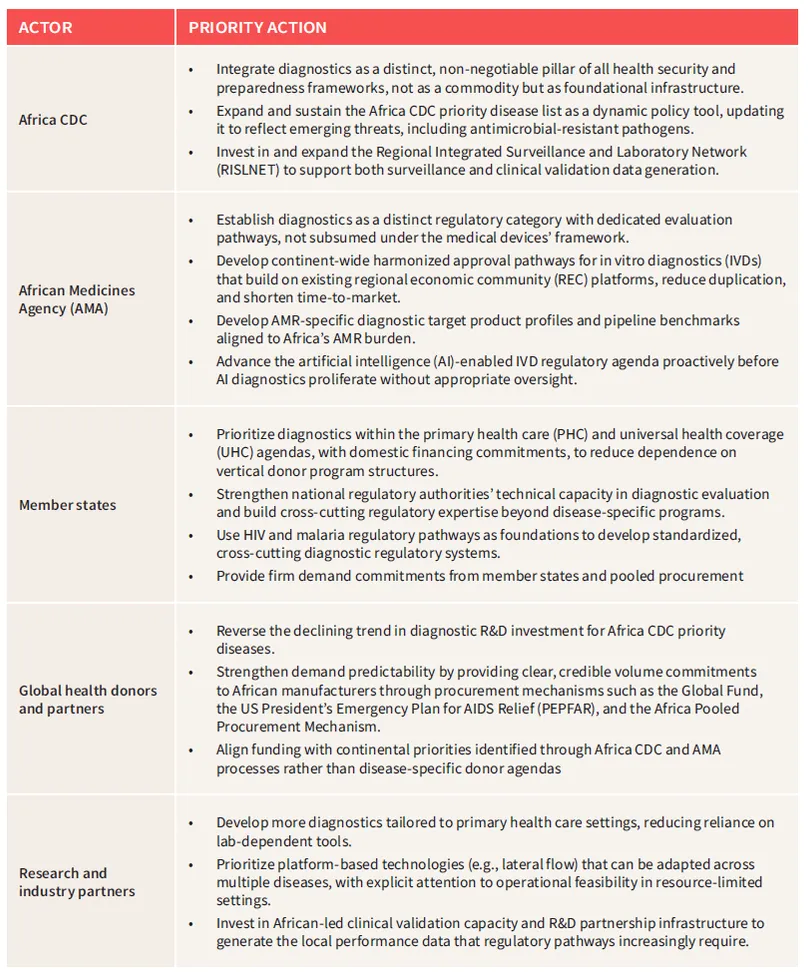

Strategic opportunities and recommendations

The following recommendations reflect the diagnostic system readiness gaps identified throughout this report. They are targeted, action-oriented, and anchored in the political commitments African institutions have already made. They do not attempt to address every dimension of the diagnostics landscape, but they address the specific issues this brief has placed in the spotlight.

Conclusion: A call to action

Africa’s diagnostic deficit is not fundamentally a product development problem. The pipeline is not empty; the institutions exist, and political commitments have been made. The central challenge highlighted in this report is the gap between commitment and capacity: between what has been approved and what is accessible, between what has been pledged and what has been funded, and between existing regulatory frameworks and the diagnostic realities they must address.

Closing this gap requires action on multiple fronts. We need to reverse the declining R&D trends for priority diseases; build regulatory systems that treat diagnostics as what they are: foundational health infrastructure, not ancillary commodities; develop firm demand frameworks that give African manufacturers the certainty they need to scale; and integrate diagnostics into primary health care and surveillance systems in ways that close the loop between innovation, deployment, and health impact.

The question is no longer whether Africa can build this ecosystem. It can. The question is whether the investment and political will required will arrive fast enough, both for the outbreaks already emerging and those still ahead, to ensure that diagnostic underinvestment does not once again define Africa’s response and expose the true cost of the deficit.

Table of contents

- Key messages

- Introduction

- Strategic context: Why diagnostics matter now

- Diagnostic R&D investment: Structurally low and declining

- The diagnostic R&D pipeline: Innovation is not translating evenly into access

- The regulatory environment: Fragmented, misaligned, and under-resourced

- Manufacturing feasibility: Capacity exists, but the ecosystem does not

- Surveillance, preparedness, and primary health care linkages

- Strategic opportunities and recommendations

- Conclusion: A call to action